The Full Federal Court decision 9 min read

The Full Federal Court decision of Minerva Financial Group Pty Ltd v Commissioner of Taxation [2024] FCAFC] 28 allowed the taxpayer's appeal, ultimately determining that Part IVA of the Income Tax Assessment Act 1936 did not apply to a trustee's failure to exercise its discretion to distribute distributable income to special unitholders which would attract a higher tax rate on the income. The decision represents a significant win for taxpayers and provides guidance on the operation of Australia's anti-avoidance rules contained in Part IVA. Particularly, the court emphasised the need to consider the 'surrounding context' to determine whether a scheme is entered into for a dominant purpose of enabling the taxpayer to obtain a tax benefit. The court's holistic approach in considering the eight factors of section 177D of the Income Tax Assessment Act 1936 is a reminder to taxpayers and advisers of the need to view transactions in their full context when considering Part IVA risk.

Key takeaways

- Group restructures will not be caught by the general anti-avoidance rule in Part IVA, provided there is sufficient evidence that the dominant purpose of the restructure was not to obtain a tax benefit. The court favoured the commercial factors supporting the distribution of only nominal amounts to the company side of the structure.

- It does not follow that Part IVA applies where a distribution is made to the trust silo of a group in accordance with constituent documents, resulting in a real benefit to unitholders and where a tax benefit is identified. Part IVA requires consideration of the surrounding context to objectively support the conclusion that there was a dominant purpose enabling the taxpayer to obtain a tax benefit.

- Transactions within a commonly owned group that are effected by way of book entries do not necessarily point to a Part IVA Scheme.

- The Commissioner did not challenge the Federal Court's conclusion that a restructure which established a staple with separate corporate and trust silos, was legitimate.

Background

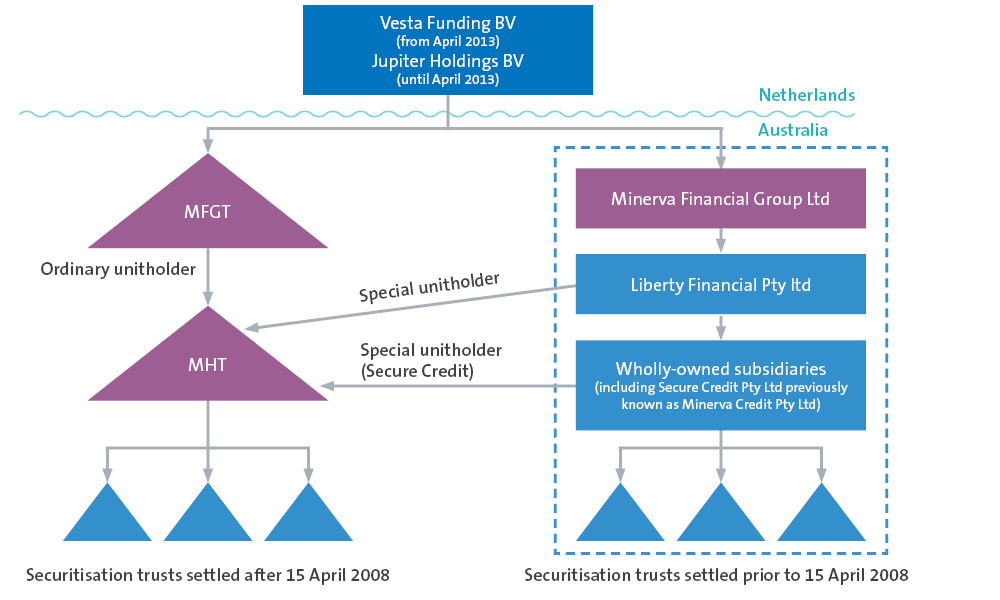

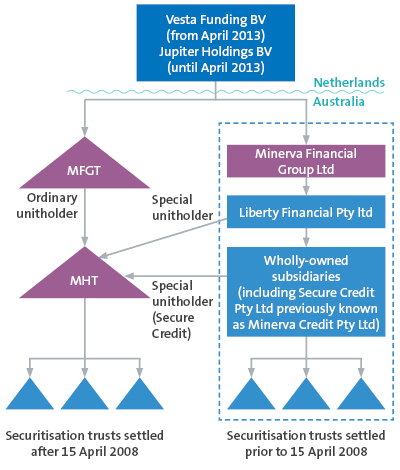

Minerva Financial Group Pty Ltd (Minerva) is a member of the group of companies and trusts known as the Liberty Group (Liberty). Liberty provided loans to its customers and obtained the capital to do so by securitising (pooling) those loans and mortgages into securitisation trusts and obtaining third-party financing. From 2002, Liberty was subject to tax on the interest income derived by the securitisation trusts at the corporate tax rate of 30%. In 2007, Liberty commenced a restructure with a view to conducting an initial public offering (IPO) of stapled securities. Liberty reorganised itself into a 'trust silo' and a 'corporate silo'. The stapled securities were to consist of a share in Minerva (and its subsidiaries) and a unit in the Minerva Financial Group Trust (MFGT) which was established with units held by Minerva that were subsequently transferred to other Liberty entities, being Jupiter Holdings BV and then Vesta Funding BV. Liberty established another unit trust, Minerva Holding Trust (MHT) which was held by MFGT and Liberty Financial Pty Ltd (LF). MHT ultimately became the holder of the residual income units and residual capital units in the special purpose securitisation trusts established by Liberty.

The judgment contains the following simplified diagram of the group following these restructure steps:

Importantly, two of the Australian companies in the corporate silo held 'special units' in the intermediate holding trust. The trustee of that trust, which was the Australian head company, had discretionary power to distribute the trust income to those companies rather than to the head trust. Exercising the discretion to distribute income to those companies effectively resulted in the income being subject to tax at the 30% corporate tax rate rather than the 10% withholding tax rate. In fact, in the relevant years the Australian head company either did not exercise the discretion (ie, no income distributed to the companies) or determined to only distribute less than 2% of the trust income to the companies.

The Commissioner determined that there had been a tax benefit obtained in connection with the scheme for each of the years 2012 to 2015 and issued assessments. Minerva's objection was disallowed, and Minerva appealed.

The primary judgment

At first instance, Justice O'Callaghan held in favour of the Commissioner, finding that the failure to exercise a power, created as part of the restructure, to make discretionary distributions from the trust group to the corporate group could only be explained by the desire to pay a lower rate of income tax. However, it was held that the overall restructuring of the loan securitisation business from a single corporate group to a corporate group and a separate trust group, which became a stapled structure, was legitimate and did not attract the operation of Part IVA. This aspect of the decision was not challenged by the Commissioner on appeal.

Our Insight on the Primary Judgment is available here.

An analysis of the Full Federal Court decision

The Full Federal Court (Besanko, Colvin and Hespe JJ) allowed Minerva's appeal, finding that Part IVA did not apply to the schemes identified by the Commissioner and setting aside the decision of Justice O'Callaghan.

The court held that the 'fallacy in this case' was that, contrary to the direction in s 177D(2), the Commissioner's decision and aspects of the primary judgment confined attention to the tax consequences of the actual and counterfactual transactions, excluding account of the 'commercial advantages and consequences obtained by parties connected with the appellant and flowing from what was done'.1 That is, although Minerva obtained a tax benefit, nothing in the 'surrounding context' objectively supported a conclusion that any party to the schemes either entered into or carried out the schemes for a dominant purpose of enabling the taxpayer to obtain a tax benefit.2

The court's judgment is a timely reminder of an orthodox approach to determining whether there is a scheme to which Part IVA applies:

- For Part IVA to apply, it must be shown that having regard to the eight matters listed in s 177D that 'it would be concluded that the person… who entered into or carried out the scheme or any part of the scheme did so for the purpose of enabling the relevant taxpayer to obtain a tax benefit in connection with the scheme'.3

- The interpretation of the word 'scheme' extends well beyond its natural meaning and includes notions of agreement, arrangement and understanding. It can also include actions or courses of action taken by one party without the involvement of another party.4

- It is the features of the scheme and surrounding circumstances which are examined in considering the s 177D factors rather than an examination of the subjective purpose or motive of a party to the scheme.5

- Section 177D does not require an inquiry as to whether a taxpayer would not have entered into the scheme 'but for' the tax benefit.6

- Where a taxpayer chooses between two transactions based on taxation considerations, it does not follow that the dominant purpose of the taxpayer was to obtain a tax benefit. Part IVA does not apply merely because the Commissioner can identify another means of achieving the commercial outcome which would have resulted in more tax being payable.7

The court's approach was to consider each of the s 177D(2) factors through a consideration of the objective facts and circumstances,8 ultimately concluding that they did not support an objective conclusion that any party entered into or carried out the schemes for the dominant purpose of obtaining a tax benefit. To summarise the key reasons for this finding:

- The trustee paid distributions in accordance with the terms of issue of the ordinary notes and the trust constitution. The objective facts were that the special unitholders had no entitlement to the income of MHT absent the exercise of the trustee’s discretion. A payment of distributions in accordance with their terms of issue is not an objective matter that points to a party carrying out the scheme for the dominant purpose of enabling the taxpayer to obtain a tax benefit.9

- The failure to exercise the discretion to pay distributions to LF did not affect the solvency, profitability or credit rating of LF. The nominal distributions to LF did not support a conclusion that a party entered into the schemes for the dominant purpose of obtaining a tax benefit.10

- MHT's distributions to MFGT, and not LF, enabled Vesta to repay interest bearing debt owed to LF and Vesta to increase its capital in MFGT. This demonstrated commercial and financial benefits beyond the tax saving.11

- The Commissioner's case rested on a comparison of the income flows before and after the restructure that assumed there was no objective reason for the change of income flows other than to secure a tax advantage. This did not engage with the unchallenged finding that the restructure was not a Part IVA Scheme and did not take into account the evidence of changed commercial circumstances, including the business need for further sources of capital.12

As to the 177D inquiry, the Full Federal Court held:13

The objective dominant purpose of a party to a scheme (such as an action or course of action) that has enabled a person to obtain a tax benefit is determined by regard to what has happened and evaluating why it has happened. Obtaining the tax benefit is not enough. Desiring the tax benefit is not enough. The obtaining of the tax benefit must have been the main object or aim of what is said to be the scheme when viewed objectively in its surrounding context.

The Court's analysis of the key s 177D(2) factors is summarised below:

The court noted that objectively there was nothing extraordinary about distributions flowing in accordance with the terms of the trust constitution.14 Importantly, the default under the constituent document was that income would be distributed to MFGT unless the trustee exercised a discretion to distribute to the special unitholders. It was also relevant that Justice O'Callaghan found that there was nothing unorthodox about recording loans in general ledgers or about loans being repaid by set-off or by ledger entries – the loan offsets did not indicate a dominant purpose of obtaining a tax benefit.15 The distributions by MHT to MFGT and the subsequent distributions by MFGT to Jupiter had real commercial consequences.

The Commissioner's contentions in relation to the second element hinged on the flow of funds as a result of the schemes, arguing that the form of the schemes was that MHT’s net income flowed predominantly to MFGT and from MFGT to Jupiter/Vesta. However the substance of the scheme, properly considered, was said to be that the funds associated with MHT’s net income flowed predominantly to LF in the form of the MHT-LF loans. The court rejected this contention stating it conflated the concept of cash or funds with the concept of income.16 The court ultimately agreed that there was no difference between the form and substance of the scheme. The substance was that MFGT benefited from its ownership of the ordinary units in MHT. The form was the same.17

The time at which the decision was made not to exercise the discretion (or to exercise it only to the extent of a nominal amount) was reflective of the terms of the MHT constitution and the need for the trustee to make a resolution by the end of the financial year.

The court emphasised the importance of viewing this factor in context, stating it must be considered holistically together with the other factors and cannot be viewed in isolation from other, commercial factors.18 In this case, it was necessary to consider that the distribution of income to Jupiter and Vesta had real economic and financial consequences to them that would not have flowed had the income been distributed to LF.19

The Commissioner argued it was reasonably foreseeable that at the time the trustee decided not to exercise its discretion to 'direct MHT’s net income' to the special unitholders in the relevant years, LF’s 'financial position' would be adversely affected because LF would have less retained earnings and a lower capital adequacy ratio.20 The court rejected this contention on the basis it discounted the financial benefits of distributions to Vesta and Jupiter by MFGT.21 This contention ignored the reality that Liberty's business was growing and additional debt and equity was raised from 2016 to support this growth.

The Commissioner also contended that the non-exercise of the discretion to distribute adversely affected LF's capital adequacy ratio. The court found this was not supported by evidence.22 LF raised capital because its business grew and not because of the non-distribution by MHT.23

The court agreed with Justice O'Callaghan that there were no other relevant consequences from the scheme.24

The court agreed with Justice O'Callaghan that the common ownership of the 'corporate silo' and 'trust silo' was a neutral factor. The court made two key points in this inquiry:

- The connection between the entities affected by the schemes (which enabled the distributions between them to be paid by intercompany loan accounts) did not, in isolation, suggest the scheme was motivated by the tax consequence.25 and;

- Once it is accepted that the trust silo was established as part of a legitimate restructure, the question becomes whether the particular way in which distributions within that structure were made thereafter attracts the operation of Part IVA.26 Justice O'Callaghan found that the creation of the trust and corporate silos was not itself a Part IVA scheme. To point to the fact that the entities affected were all connected casts no light on whether a party to any of the schemes had the requisite dominant purpose.27

Footnotes

-

Minerva Financial Group Pty Ltd v Commissioner of Taxation [2024] FCAFC 28 [121].

-

Ibid [123]

-

Ibid [60].

-

Ibid[1].

-

Ibid[63].

-

Ibid [68].

-

Ibid[60].

-

Ibid[69].

-

Ibid[76].

-

Ibid[110].

-

Ibid[109]; [121].

-

Ibid[122].

-

Ibid[65].

-

Ibid[76].

-

Ibid[74]-[76].

-

Ibid[88]-[89].

-

Ibid[86].

-

Ibid[100].

-

Ibid[101].

-

Ibid[103].

-

Ibid[106].

-

Ibid[108].

-

Ibid[107].

-

Ibid[115].

-

Ibid[117]-[119].

-

Ibid[120].

-

Ibid.