After strong industry feedback, the CCIV regime is ready to commence on 1 July 2022 17 min read

Nearly five years after the Federal Government first released the exposure draft legislation for the new corporate collective investment vehicle (CCIV), on 10 February 2022 the Corporate Collective Investment Framework and Other Measures Bill 2021 (the CCIV Bill) was finally passed by the House of Representatives and the Senate. During these five years, there were multiple rounds of draft legislation and public consultation and the CCIV regime, particularly the tax component, was re-worked in response to strong industry feedback. We now have the final CCIV regime, ready to commence on 1 July 2022 following royal assent. We have summarised the key features of the CCIV regime below.

Key takeaways

- A CCIV is a new type of company limited by shares. The CCIV will be a single legal entity and must have at least one sub-fund.

- Sub-funds will not have separate legal personality but each sub-fund's assets and liabilities will be segregated from the assets and liabilities of other sub-funds. This feature may be of particular interest to fund managers who currently create multiple classes of units in unit trusts to obtain a similar effect but with the risk of cross-class liability.

- A CCIV must have a corporate director which, like a responsible entity, must be a public company and must have an appropriate Australian financial services licence (AFSL) (a new AFSL authorisation will be introduced). There is no longer a requirement for retail CCIVs to have a depositary to hold on all the assets of the CCIV.

- Certain features of the existing managed investment scheme (MIS) regime will be replicated for CCIVs to ensure regulatory parity between the two frameworks. In other instances, the ordinary company rules under the Corporations Act will apply to the CCIV. While a lighter touch regulatory approach has been adopted for wholesale CCIVs, all CCIVs (including wholesale CCIVs) must be registered with ASIC, which means they are more heavily regulated than unregistered wholesale MISs. This may mean that the CCIV may be less attractive to wholesale fund managers and their investors.

- A sub-fund may cross-invest (ie acquire shares in another sub-fund in the same CCIV) and a single asset may be allocated across multiple sub-funds, in each case subject to certain conditions. These features provide greater flexibility to create different investment structures more efficiently.

- There have been significant changes to the CCIV tax regime since the release of the original exposure draft legislation with Parliament ultimately settling on a tax framework for CCIVs, and their investors, that is intended to align with the existing framework for 'attribution managed investment trusts' (AMIT).

- In particular, the tax rules create a 'statutory fiction' so that each sub-fund of a CCIV is deemed, for tax purposes, to be a separate unit trust – the CCIV is (notionally) the trustee of the sub-fund and investors in the CCIV that hold shares referrable to the sub-fund are the beneficiaries under the trust. Generally speaking, investors should be taxed on an attribution 'flow through' basis for income derived by a qualifying sub-fund of a CCIV.

- On the whole, the adaptation of the AMIT rules should provide a more familiar and pragmatic starting point for the taxation of CCIVs. There are, however, certain residual issues – particularly where a sub-fund does not meet the conditions to qualify as an AMIT – which may pose problems in practice, and to that end, the ATO is expected to issue more detailed practical guidance on how some of rules may apply.

- Moreover, the statutory fiction that is created by the tax rules – whereby the 'segregated' assets, liabilities and business of a company are treated, for tax purposes, as a separate trust estate – may have unintended interactions with other existing tax regimes. These will only become clear once the rules have been tested in practice.

- Unlike in earlier iterations of exposure draft legislation, Treasury did not introduce a transitional regime which would allow existing funds tax roll-over relief to restructure into a CCIV. Nor, at this stage, have there have been any announced developments by States or Territories in relation to the availability of stamp duty relief (and whether the statutory fiction created for tax purposes would be respected for stamp duty purposes). The absence of tax and duty relief is likely to be prohibitive for many existing funds wishing to restructure into a CCIV model.

Where it started

The concept of a new corporate collective invesmtent vehicle was first introduced in November 2009 in the Johnson Report which recommended, among other matters, that in order for Australia's managed funds sector to become more competitive, Australia needed a collective investment vehicle that would provide flow-through tax treatment and would be more internationally recognisable than the current MIS.

The government accepted this recommendation in the 2016-2017 Budget where it announced its intention to produce a new regulatory framework for a CCIV regime, and in September 2017, we saw the first exposure draft legislation for the CCIV.

The CCIV framework was developed having regard to equivalent vehicles used in other jurisdictions while still having features similar to the existing MIS structure. The complexity of integrating a new type of company that effectively has hybrid company and MIS-like features into an existing regulatory landscape was evident in the submissions that were received during the consultation period. In particular, the tax treatment of CCIVs had fundamental issues which required some time to iron out. However, we now have a CCIV framework which, for the most part, has addressed the key concerns in the earlier drafts. This is discussed in more detail below.

Overview of the CCIV regime

Legal framework

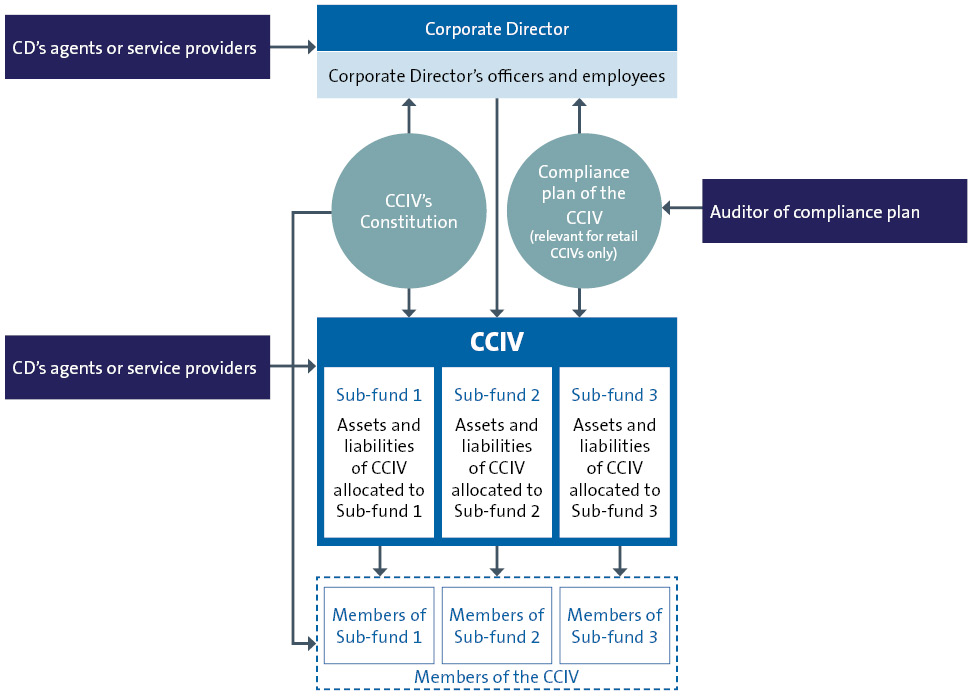

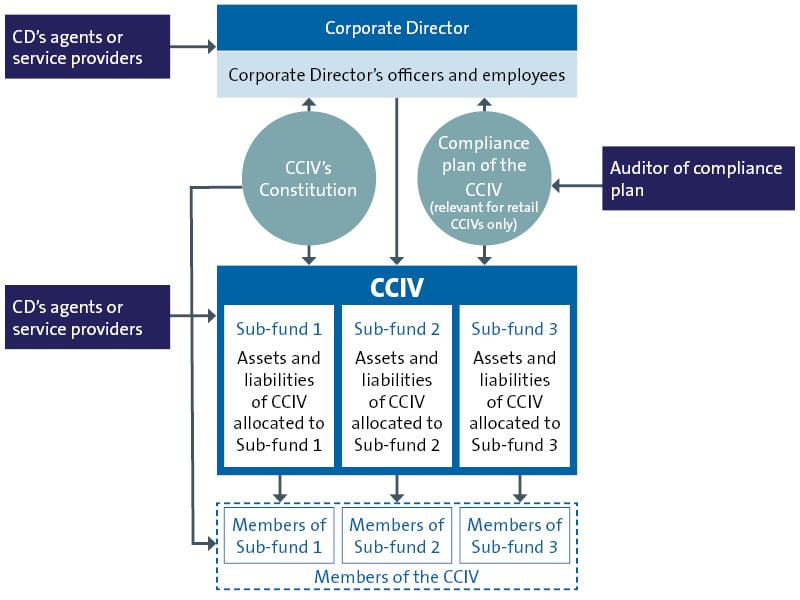

CCIVs will have the legal form of a company limited by shares with most of the powers, rights, duties and characteristics. As a type of company, a CCIV has the legal capacity and powers of an individual and a body corporate. However, the CCIV will only have a sole director (a corporate director) and must not have any other officers or employees (other than a director or a receiver, liquidator or a trustee or other person administering an arrangement between the CCIV and someone else).

In contrast to other types of companies, a CCIV is an umbrella vehicle that is comprised of one or more sub-funds. Each sub fund is comparable to an individual unit trust which is commonly used under the existing MIS regime.

The primary governing document for a CCIV is the constitution. Unlike other company types, a CCIV must have a constitution and not rely on the replaceable rules set out in the Corporations Act. Additionally, as in the MIS regime, the constitution of a retail CCIV must make adequate provision for certain matters (for example, the handling of complaints made by investors). A wholesale CCIV must have a constitution but there are no prescribed contents.

Retail CCIVs must also have a compliance plan, which meets the legislative requirements (as with the MIS regime, there are only basic prescribed requirements) and a compliance plan auditor.

Unlike the MIS regime, where wholesale schemes need not be registered with ASIC, both retail and wholesale CCIVs must be registered with ASIC.

To establish a CCIV, it must be registered with ASIC through a registration process that largely mirrors the existing process in place for other companies but requires a copy of the CCIV's constitution to be provided to ASIC and, for retail CCIVs, a copy of the compliance plan. In earlier iterations of the Bill, we have made submissions that, in the same way that the requirement to lodge a constitution does not apply to propriety companies, the requirement to lodge a constitution should be restricted to retail CCIVs. Unfortunately, this has not been adopted and may hinder adoption of the CCIV model amongst fund managers who operate wholesale MISs.

Once registered, a CCIV may not convert to another type of company nor can another type of company change to a CCIV.

The director of a CCIV must be a public company with an AFSL authorising it to operate a CCIV (see below). Additionally, the corporate director for a retail CCIV must itself have at least half of its directors as external directors which is a distinct departure from the MIS regime. Under the MIS regime, a responsible entity may have less than half its directors as external directors (and may have no external directors) provided it establishes an independent compliance committee. The policy motive for mandating external directors for directors of CCIVs is to bring a degree of detached supervision which is expected to enhance the standard of corporate governance (an area which ASIC has identified in its 2021-2025 Corporate Plan as a key focus).

The corporate director of a CCIV is generally responsible for the conduct of the CCIV. This reflects the fact that a CCIV must not have any employees and its only director is the corporate director. Accordingly, the consequences of contravening a commonwealth criminal offence or civil penalty provision by a CCIV do not apply to the CCIV. Instead, the corporate director of the CCIV at the time of the offence or contravention is taken to have committed the offence or contravened the provision and is therefore liable for any associated fine or penalty.

The duties and obligations of directors of CCIVs align more closely to those of a responsible entity than to those of a director of another company type. However, unlike the MIS regime where trustees of unregistered schemes do not have specific duties and obligations applicable to them (other than for licensing obligations), corporate directors of wholesale CCIVs will also be subject to such duties and obligations. While the CCIV regime permits some of the additional duties and obligations owed by a corporate director of a wholesale CCIV to be expressly excluded under the CCIV constitution, corporate directors of wholesale CCIVs will still be subject to some regulatory oversight.

Financial services may be provided by the corporate director or the CCIV itself (being a legal entity). As noted above, a corporate director will be required to hold an AFSL which authorises it to 'operate the business and conduct the affairs of a CCIV', irrespective of whether the corporate director will be operating a retail or wholesale CCIV. Financial services which are provided by the CCIV are covered by the corporate director's AFSL and accordingly, the CCIV is exempt from the requirement to hold an AFSL itself.

Even though a CCIV itself does not hold an AFSL, the CCIV is deemed to be a professional investor (and therefore, a wholesale client for the purposes of the Corporations Act) for so long as the corporate director holds an AFSL.

Retail CCIVs are subject to a regulatory framework that encompasses additional regulatory protections necessary for retail investors, while there is a lighter touch regulatory approach to wholesale CCIVs. Notification must be given to ASIC as to whether a CCIV is retail or wholesale.

A CCIV will be considered a retail CCIV if it satisfies one of the three following retail CCIV tests:

- at least one member of the CCIV is a 'protected retail client'. A person is a protected retail client if they acquire securities in the CCIV as a retail client, unless the person is 'associated' with the CCIV, or where the person acquires the security under the small scale personal offer exemption;

- at least one person is a 'protected client under a custodial arrangement'. A person is a protected client under a custodial arrangement if the person acquires the securities in the CCIV under a 'custodial arrangement', but would have been a retail client if there was a equivalent direct acquisition of the securities by that person, and the person is not associated with the CCIV; or

- at least one member is a 'protected member of a passport fund'. This applies where the sub-fund is an Australian passport fund and the person became a member after the sub-fund became an Australian passport fund or on the expectation that the sub-fund would become an Australian passport fund.

A CCIV that is not a retail CCIV is a wholesale CCIV.

A sub-fund of a CCIV is all or part of the business of the CCIV that is registered as a sub-fund with ASIC. The first sub-fund is registered as part of the broader registration of the CCIV itself, and subsequent sub-funds may be created by the CCIV by lodging an application to register the sub-fund with ASIC through a streamlined registration process.

Each sub-fund is not a separate legal entity but the assets of each sub-fund are strictly segregated from all other parts of the CCIV's business and can only be applied for specific purposes (eg meeting liabilities of that particular sub-fund).

While sub-fund like structures can be established under the existing MIS (unit trust) regime by creating different classes of units, with assets and liabilities of a unit in a particular class being referable to that class, there is no legal segregation of assets and liabilities on a class by class basis. This means that all assets of the trust are potentially available to meet the liabilities of any given class, even where the assets applied to meet the class liability are not referable to that class. A key feature of the CCIV structure is that such cross-class liability risk is removed as the assets of each sub-fund can legally only be applied for purposes relating to that specific sub-fund.

A CCIV can only issue a share or debenture (securities) which is referable to a specific sub-fund. This means that the rights attaching to the security must relate to the assets of that specific sub-fund. However, a CCIV may issue multiple classes of securities for each sub-fund.

The types of shares that a CCIV may issue are the same as other companies: ordinary shares, preference shares and redeemable shares. See below re redemptions of shares.

CCIVs may have unlimited share capital (i.e. open-ended) or may have fixed or limited share capital (ie closed ended).

Shares in a retail or wholesale CCIV can be redeemed if:

- the relevant shares are redeemable shares or redeemable preference shares;

- the redemption is on the terms on which the shares are issued; and

- the sub-fund to which the shares relate is not insolvent immediately before the redemption and there are reasonable grounds for suspecting that the sub-fund would not become insolvent immediately after redemption.

Further to the above, for retail CCIVs, additional requirements also apply depending on whether the sub-fund to which the shares relate is liquid or not liquid. These additional requirements largely mirror the requirements for registered schemes, particularly regarding the additional 'withdrawal offer' type regime that applies where the sub-fund is not liquid.

The redemption regime which applies to all CCIVs has been modelled on the requirements for redemptions of redeemable preference shares in a company, but with the added flexibility such that the redemption in a CCIV does not need to be paid out of the profits or proceeds of a new share issue. While these 'base level' redemption requirements are not particularly onerous, some wholesale investors may be less attracted to the CCIV structure when compared to the existing unregistered MIS structure as redemptions from the latter are not at all regulated by the Corporations Act.

Assets of a CCIV may be held by the CCIV itself or by engaging an asset holder such as a custodian to hold the assets on behalf of the CCIV.

While the appointment of an external asset holder will create a trust relationship between the asset holder and the CCIV, the CCIV Bill is clear that there is no intention of making a CCIV or its corporate director a trustee of the assets held by a CCIV. Thankfully, the previous requirement for mandatory depositaries (independent third parties which hold the assets of a CCIV) for retail CCIVs has been scrapped, meaning there is less regulatory burden for establishing a retail CCIV.

Generally speaking, money or property acquired by a CCIV forms part of the assets of the sub-fund if the money or property was acquired using the assets of that sub-fund. However, where the money or property being acquired relates to the business of more than one sub-fund, the corporate director must determine the proportion of the money or property which is to be allocated across the relevant sub-funds. Where a single item of property forms part of the assets of two or more sub-funds and is indivisible (eg a share or a unit), that property must be converted into money or other fungible assets so that it can be allocated across the relevant sub-funds.

Similar liability allocation rules also apply to sub-funds.

A new development is that a CCIV may generally engage in cross-investment between its sub-funds, meaning a CCIV can, in respect of one sub-fund, acquire shares that are referable to another sub-fund. However, the proposed regulations prohibit 'circular' cross-investment – ie the acquiring sub-fund must not acquire shares in the other issuing sub-fund. Doing so would result in the acquiring sub-fund obtaining shares in itself. This may occur where the issuing sub-fund already holds shares in the acquiring sub-fund as an asset (either directly or through a series of interposed sub-funds).

A consequence of cross-investment is that a CCIV becomes a member of the issuing sub-fund as it is the legal entity holding the shares in the issuing sub-fund. In such circumstances, where the CCIV is entitled to vote on a resolution at a meeting of the member of the issuing sub-fund, the draft Corporations and Other Legislation Amendments (Corporate Collective Investment Vehicle Framework) Regulations 2021 (the Regulations) prescribe that the CCIV is only entitled to vote where the members of the acquiring sub-fund pass a special resolution determining how the CCIV is to vote.

The ability to cross-invest across sub-funds in a CCIV provides greater flexibility to create different investment structures in a more efficient manner and is another improvement in the CCIV regime following feedback on previous exposure drafts of the bill. The EM explains that this approach is to align the CCIV regime with other international corporate collective vehicles and ensures that a CCIV can utilise funds management structures such as a master-feeder structure (where a CCIV establishes a sub-fund that holds a certain asset class and then creates additional sub-funds with varying levels of exposure to that initial sub-fund) or a hedging structure (where one sub-fund holds core assets and additional sub-funds holds relevant hedging instruments and shares in that core sub-fund).

The provisions regulating meetings of CCIVs (which can be a meeting of the members of the whole CCIV or a particular sub-fund of the CCIV) are substantially the same as the meeting provisions in respect of registered schemes.

An important distinction is that the meeting provisions for CCIVs apply to both retail and wholesale CCIVs. Under the MIS regime only registered schemes are required to hold meetings in accordance with the Corporations Act, whereas wholesale scheme meetings are specifically are largely ungoverned. This is another potential barrier for adopting the CCIV model by wholesale fund managers as they will be required to abide by more stringent meetings requirements compared with the MIS regime.

At this stage, only a retail CCIV with a single sub-fund or sub-fund of a retail CCIV which only has that one sub-fund may be included in the official list of a prescribed financial market in Australia. However, these restrictions do not apply in respect of quoting a share in a CCIV on a financial market such as AQUA – a share in a CCIV may be quoted, regardless of the number of sub-funds it may have, provided it satisfies the quotation requirements of the financial market.

In earlier exposure drafts, a CCIV was prohibited from being listed on a financial market and accordingly, the current position is a welcomed improvement. The EM also notes that the listing of retail CCIVs with more than one sub-fund, or the listing of multiple sub-funds of a retail CCIV, will be considered in the future once the CCIV regime is operating. It is also worth noting that on 1 February 2022, the ASX released its consultation paper seeking feedback on the changes that the ASX are proposing to the ASX Listing Rules and the ASX Operating Rules to facilitate the listing and quoting of CCIVs and sub-funds.

Retail clients who acquire a share in a CCIV must be provided with a PDS. This means that Part 7.9 rather than the disclosure requirements in Chapter 6D will apply to shares in a CCIV. The content requirements for the PDS of a CCIV are largely consistent with the requirements for PDSs of registered schemes. Further, the Regulations also introduce a concept of 'simple sub-fund products' which is intended to be analogous to interests offered in simple MISs. A simple sub-fund product is a security in a sub-fund of a retail CCIV where at least 80% of the assets of that sub-fund are liquid assets. Such sub-funds will be able to benefit from simple PDS regime, similar to that which applies to simple MISs.

If a CCIV is a disclosing entity, it must comply with the continuous disclosure requirements (similar to a MIS which is a disclosing entity).

A corporate director of a retail CCIV may lodge an application to register a sub-fund as an Australian passport fund. The Asia Region Funds Passport (ARFP) regime was another recommendation made by the Johnson Report to provide a multilateral framework allowing eligible funds to be marketed across member countries with less regulation. The introduction of a CCIV would assist in marketing Australian funds offshore, given it has a more internationally recognisable structure. However, given the limited uptake of the ARFP regime to date, it is uncertain whether using a CCIV would mean there is much increased interest in the ARFP regime.

Tax framework

General tax treatment

The general tax objective of the new CCIV regime is ensuring that members can achieve attribution and flow-through of income from a CCIV through the AMIT regime. Therefore, the new CCIV rules incorporate provisions which deem each sub-fund of a CCIV to be a separate trust for tax purposes. This has the effect that:

- the assets, liabilities and business referable to a sub-fund are treated as a separate unit trust (known as a ‘CCIV sub-fund trust’);

- the CCIV is treated as the trustee of the CCIV sub-fund trust; and

- members who hold shares in the CCIV that are referable to a sub-fund are treated as the beneficiaries of the CCIV sub-fund trust.

The assets, liabilities and business that are referable to a sub-fund will constitute the trust property which is held on trust for the benefit of the relevant beneficiaries of the CCIV sub-fund trust. The assets, liabilities and business of one sub-fund cannot be treated as belonging to any other sub-fund for tax purposes.

The CCIV will be treated for tax purposes as if it were a different tax entity in its capacity as trustee of each trust, with distinct responsibilities to meet the obligations of a trustee under the taxation law in respect of each CCIV sub-fund trust.

By deeming each sub-fund to be a separate unit trust, the new tax laws are intended to allow a sub-fund to pass threshold criteria of the AMIT regime (as amended for CCIVs) so that it and its members can be eligible for attribution flow-through taxation treatment. If the CCIV does not meet the amended AMIT eligibility criteria, the general trust taxation rules will apply. Notwithstanding its corporate structure, a CCIV will not be taxed as a company (unless the public trading trust rules under Division 6C apply to the CCIV). This has various implications for the taxation of the CCIV, including, for example, that the trust loss (and not the company loss) provisions should apply.

The deeming principle applies for the purposes of all taxation laws unless expressly excluded, including Australia's international tax treaty network. The specific implications of this statutory fiction in its interactions with existing tax regimes will become apparent as the new rules are tested in practice.

The deeming principle has no application outside of the tax law, and does not act to create a trust for any other purposes

Under the new law, a CCIV sub-fund trust that meets a modified version of the AMIT eligibility criteria will be treated as an AMIT for tax purposes. The requirements for a CCIV sub-fund to qualify as an AMIT, as modified, are broadly that:

- the sub-fund meets the requirements to be a MIT for an income year, meaning that it:

- must be an Australian resident, or have central management and control in Australia (noting that the sub-fund will be treated as a trust when testing its residency, not a corporation);

- must not carry on or control a trading business (noting that there are no amendments to this test in Division 6C under this new law, meaning the traditional complexity of confirming this point remains); and

- it satisfies the widely held requirements and the closely held restrictions during the income year (noting that neither of these tests are materially amended);

- although the requirement to be a MIS has been removed due to its incompatibility with the CCIVs corporate structure, a CCIV must satisfy a new, similar requirement that a sub-fund (in its legal capacity) must be used for collective investment by pooling contributions of members as consideration for a return on those investments.

Some of these requirements equally apply to the CCIV sub-fund trust’s ability to be a ‘withholding MIT’ (under section 12-383 in Schedule 1 to the Taxation Administration Act 1953 (Cth)).

A qualifying sub-fund will automatically be treated as an AMIT for tax purposes. There is no election mechanism, which also means there is no ability for a CCIV to opt-out of AMIT treatment.

If a CCIV sub-fund trust fails to meet the AMIT requirements due to temporary circumstances that are outside the control of the trust, it can continue to be treated as an AMIT in relation to the income year if it is 'fair and reasonable' to do so. In determining whether it is 'fair and reasonable' to do so, certain factors prescribed by the legislation must be considered by the trust.

If a CCIV sub-fund trust qualifies as an AMIT, it will have the following features:

- (fixed trust) each CCIV sub-fund trust is deemed to have fixed trust status;

- ('unders and overs') the CCIV sub-fund trust can use the ‘unders and overs’ regime to reconcile a variance between the amounts attributed to members of the CCIV sub-fund trust for an income year, and the amounts that should have been attributed in the same way that an AMIT can. This avoids the need for investors to amend prior year assessments;

- (capital election) the CCIV sub-fund trust can elect into capital account treatment for its gains and losses made on various assets;

- (trustee tax) the CCIV as trustee is responsible as trustee under the AMIT rules and may be liable to pay tax in certain circumstances; and

- (non-arm's length income) the non-arm’s length income rule for MITs (in Subdivision 275-L) also applies to a CCIV sub-fund trust.

However, if the CCIV sub-fund trust does not satisfy the modified AMIT eligibility criteria, it will be taxed under either Division 6 or Division 6C of the 1936 Act, as relevant.

It is noted that certain widely-criticised features of previous exposure drafts, including the administrative penalty on unders and overs, have been removed.

If a CCIV sub-fund trust satisfies the modified AMIT eligibility criteria, investors (ie, members of the CCIV who are beneficiaries of the particular CCIV sub-fund trust) will be impacted as follows:

- (flow-through treatment) the CCIV sub-fund trust will receive flow-through tax treatment, meaning that investors will generally be taxed as if they had invested directly in the underlying assets;

- (attribution) for income tax purposes, the CCIV sub-fund trust is able to attribute amounts of assessable income, exempt income, non-assessable non-exempt income and tax offsets to members on a fair and reasonable basis; and

- (original source and character retained) amounts that are attributed to members will retain their original source and character and will not be treated as a dividend (including for treaty purposes) unless the amount had the character of a dividend when it was derived or received by the attribution CCIV sub-fund trust.

The new laws also deem an investor to have an individual interest in the exempt income or non-assessable non-exempt income (that is, tax preferred income) of the CCIV sub-fund trust, in order to clarify that beneficiaries of the CCIV sub-fund trust can only be presently entitled to the income of the trust under Subdivision 195-C.

Under the AMIT rules, in circumstances where the amount of assessable income attributed to a member differs from the amount of money actually paid in an income year, the capital gains tax (CGT) cost base of the member’s interest is adjusted to ensure that assessable member income is only taxed once. In the event that more income is attributed than is distributed then the cost base is increased, and vice versa.

The CCIV is specifically required to provide investors with a notice setting out the information that the investor needs in order to manage its Australian income tax position within three months of the end of the financial year.

The Commissioner has a discretion to extend this three month timeframe.

Where a CCIV sub-fund does not qualify as an AMIT, the investors are generally taxed on their share of the net income of the trust (consistent with the principles in Division 6 of the 1936 Act).

The new rules, however, introduce specific deeming rules regarding an investor's 'fixed entitlement' and 'present entitlement'.

Under the new laws, a beneficiary of a CCIV sub-fund trust will have a prescribed 'fixed entitlement' to a share of income and capital of the trust which should be broadly pro rata to the rights attached to the beneficiary's shareholding. Further, beneficiaries are taken to have a present entitlement to a share of the income of the trust which is equivalent to the 'profit' of the sub-fund that was (or is) payable to the beneficiary by way of a dividend declared during or within three months of the end of the financial year.

These rules mean that where the sub-fund of a CCIV does not qualify as an AMIT, it may be taxed on a different basis to a managed investment scheme in similar circumstances. Namely, for the managed investment scheme, the constitution or trust deed (rather than the tax rules) would generally determine a beneficiary's present entitlement to income of the trust.

The Commissioner has no discretion to extend the three month window for payment of dividends, making it important that CCIVs act promptly to ensure any dividends are paid within that window.

The formula for calculating fixed entitlement has been deliberately matched to the rights of the share, rather than proportionate holding, to reflect that there may be multiple classes of share per sub-fund (which could have differing characteristics).

If a CCIV sub-fund trust does not satisfy the AMIT eligibility requirements for a particular income year, the CCIV and its investors will be taxed either under Division 6 (general trust provisions) or Division 6C (trading trust provisions) of the 1936 Act. As the trust tax rules may apply to CCIVs, it will be important from a practical perspective that CCIV constitutions include the necessary clauses to allow those rules to be applied.

If a CCIV sub-fund trust is to be taxed under Division 6:

- investors will be taxed on the share of the net income of the trust to which they are 'presently entitled'. As set out above, the investors will have a deemed present entitlement based on dividends declared during or within three months of the end of the income year. This is an important improvement from earlier drafts, which only deemed a present entitlement for amounts actually paid;

- income of the trust which is not declared as part of a dividend will be income to which no beneficiary is presently entitled, and therefore taxable to the CCIV; and

- if a dividend is declared and there was an accounting loss for the sub fund then the dividend will be taken to have been paid out of the trust corpus and there may be capital gains tax consequences.

If a CCIV sub-fund trust is to be taxed under Division 6C as a 'public trading trust', it will be taxed as a company in accordance with the provisions of that Division. Importantly, a CCIV that is taxed under this Division will not be prohibited from making frank distributions to investors. This is a welcome improvement over previous drafts of the legislation.

The CCIV legislation introduces a requirement that trust income of the CCIV be calculated for tax purposes using the concept of the 'profit' of the sub-fund as it was or would be recorded in financial statements (depending on whether the CCIV is a retail or wholesale CCIV). In this context, the income must be calculated with reference to accounting standards. If the income of the trust would be an accounting loss, the new law substitutes that for trust income of nil.

Similar to the present entitlement rules discussed above, this is a limitation on the standard powers of the trustee to determine the trust income in accordance with the terms of the relevant trust deed. Although there are concerns that this construction could lead to additional taxation of investors, Treasury has rationalised this anomaly on the basis that a CCIV is essentially a corporate entity and that the rules are not inconsistent with the existing regime for funds. The ATO has flagged that it will be working through public advice and guidance which may provide further detail on how these provisions may work in practice.

Future expectations

Currently, there is no tax roll-over relief available for the transitioning of investment vehicles which are currently structured as MISs/AMITs into CCIVs. It is anticipated that, without a transitional regime, a change of an investment vehicle from a MIS into a CCIV would trigger a tax event with potential CGT and other tax consequences.

Treasury has commented that appropriate forms of transitional relief are being considered.

Similarly, there is currently no stamp duty relief in any of the Australian States or Territories for the restructure of MISs into CCIVs, and no clear guidance about how CCIVs will be treated for stamp duty purposes. Although this is the province of the individual States of Territories, a lack of stamp duty relief will likely be prohibitive for certain existing fund managers looking restructure their funds into a CCIV.

It is expected that the States and Territories will begin releasing draft legislation determining how the duties regimes will apply to CCIVs for all purposes, including during a restructure, now that the income tax regime has been established.

What's next?

Following royal assent, the CCIV regime will commence on 1 July 2022. That said, we are still waiting to see the outcome of the Regulations (consultation closed on 21 January 2022) as well as ASIC policy and ATO guidance on the regime. If you would like to discuss how a CCIV may work for you, please contact us and we can help you navigate the new regime.