The use of special dividends in public M&A 10 min read

The current Australian M&A landscape continues to be marked by a tough valuation environment, with bid-ask spreads, interest rate uncertainty and an uncertain macroeconomic backdrop making the completion of transactions difficult. The traditional tools available in private deals to address these issues (think earnouts, deferred consideration) are not so simply implemented in public transactions. Amidst these complexities, we are observing bidders and targets increasingly turn to the use of special dividends in their dealmaking toolkit to bridge that valuation gap. The use of special dividends may improve the value proposition of a bidder's offer by releasing accumulated profits and franking credits to existing shareholders prior to the sale completing.

In this Insight, we consider the use of special dividends in public transactions in providing parties with price flexibility and delivering greater value to shareholders, ultimately, to bridge valuation gaps and deliver successful transactions.

Where and how have they been used in practice?

Special dividends are increasingly being utilised by bidders and targets. We call out below some of the more recent cash and scrip transactions in the market that have included special dividends.1

| Blackmores 2023 | ||

|---|---|---|

| CONSIDERATION: $95.00 per share reduceable by ordinary dividends and a special dividend equal to $3.29 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $1.41 per share | $96.43 per share |

| Invocare 2023 | ||

| CONSIDERATION: $13.00 per share reduceable by ordinary dividends and a special dividend equal to $0.60 per share (plus scrip alternative) | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.15 per share | $13.25 per share |

| Newcrest 2023 | ||

| CONSIDERATION: 0.400 Newmont shares per share not reduceable by ordinary dividends and a special dividend equal to US$1.10 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| May be fully or partially franked subject to conditions | – | $29.27 per share (implied) |

| Oz Minerals 2022 | ||

|---|---|---|

| CONSIDERATION: $28.25 per share reduceable by ordinary dividends and a special dividend equal to $1.75 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.75 per share | $29.00 per share |

| Crestone 2022 | ||

| CONSIDERATION: $5.15 per share reduceable by ordinary dividends and an initial special dividend equal to $0.08 per share and not reduceable by a further special dividend equal to $0.03 - $0.06 | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | Not disclosed | |

| Uniti 2022 | ||

| CONSIDERATION: $5.00 per share reduceable by ordinary dividends and a special dividend equal to $0.105 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.05 per share | $5.05 per share |

| Huon Aquaculture Group Limited 2022 | ||

| CONSIDERATION: $3.85 per share reduceable by ordinary dividends and a special dividend equal to $0.125 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.05 per share | $3.90 per share |

| Australian Pharmaceutical Industries 2022 | ||

| CONSIDERATION: $1.55 per share reduceable by ordinary dividends and a special dividend equal to $0.03 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.013 per share | $1.563 per share |

| Bingo Industries 2021 | ||

| CONSIDERATION: $3.45 per share reduceable by ordinary dividends and a special dividend equal to $0.117 per share (plus mixed cash-scrip alternative) | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | 0.05 per share | $3.50 per share |

| 1300 Smiles 2021 | ||

| CONSIDERATION: $8.00 per share reduceable by ordinary dividends and a special dividend equal to $1.00 per share (plus contingent note alternative) | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.27 per share | $8.27 per share |

| Australian Pharmaceutical Industries 2021 | ||

| CONSIDERATION: $1.55 per share reduceable by ordinary dividends and a special dividend of up to $0.03 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.013 per share | $1.563 per share |

| rhipe Limited 2021 | ||

| CONSIDERATION: $2.50 per share reduceable by ordinary dividends and a special dividend equal to $0.13 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.056 per share | $2.556 per share |

| RXP Services 2020 | ||

| CONSIDERATION: $0.55 per share reduceable by ordinary dividends and a special dividend equal to $0.05 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.0214 per share | $0.5714 per share |

| Saracen Mineral Holdings Ltd 2020 | ||

| CONSIDERATION: 0.3763 per Northern Star shares per share not reduceable by a special dividend of $0.038 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.016 per share | |

| OptiComm Ltd 2020 | ||

| CONSIDERATION: Implied value of $6.67 comprise of $5.20 and 1.07 Uniti shares per target share reduceable by ordinary dividends and a special dividend of $0.10 per share | ||

| Frankability of dividend | Franking credits attaching to dividend | Implied value to qualifying target shareholders (including franking credits) |

| Fully franked | $0.043 per share | $6.713 per share (implied) |

Navigating special dividends

With these use cases in mind, we set out below certain key issues and considerations that bidders and targets alike must grapple with when adopting special dividends in transactions.

Conditionally

The attractiveness of a bidder's offer to target shareholders can be correlated with the degree of certainty bidders and targets can afford shareholders at announcement that a special dividend will be declared and paid. Equally, target boards should not fetter their discretion, or commit at announcement to declaring a special dividend (particularly where the period between announcement and payment of a special dividend may be significant, eg a number of months). This is a balancing of competing interests. By way of example, Invocare's announcement of its non-binding indicative offer and exclusivity arrangements with TPG suggested the amount, declaration and frankability of any special dividend are only 'expected'. While certainty may have its allure, conditionality should be preserved to navigate the risk of the unexpected between announcement and declaration. Simply put: directors should exercise caution when committing to the payment of future dividends that may at that time put them in breach of their directors' duties or at law.

Form of funding

Target company liquidity may be a concern when committing to the payment of special dividends. However, in meeting these concerns, target boards may consider utilising forms of bidder financing. Such funding waylays the potentially significant outlay of funds associated with a target-funded dividend and can assist to avoid any apparent risk of material prejudice to the company, its shareholders or creditors. A bidder-funded dividend, as in the Uniti scheme, by way of consideration in advance or unsecured loan and which can be provided on desirable terms (eg interest-free, unsecured and subordinated to the target's other debt facilities) is a desirable option (and by no means the only option) for target boards to consider. But, beware the tax pitfalls with bidder-funded special dividends, as discussed below.

Whether special dividends are a form of prohibited 'financial assistance' by targets to bidders remains an open question that needs to be considered. Even so, various structuring methods can and do navigate the threshold issue of whether special dividends are prohibited 'financial assistance.' Indeed, prior agreement with target boards that officeholders provide evidence as to financial health, adequate target board resolutions or the adoption of a target shareholder approval 'whitewash' are means by which parties can obtain comfort.

Tax considerations

Typically, target companies attach franking credits to the special dividend so that it is fully or partly franked. The use of special dividends can improve the bidder's offer by allowing qualifying Australian tax resident shareholders to obtain the benefit of franking credits in the target.

ATO ruling

Target companies will usually apply to the ATO to confirm (by way of a class ruling) how a franked special dividend paid in connection with the scheme would be subject to tax for target shareholders. In particular, the ruling would usually consider the following key issues:

- First, does the special dividend form part of the 'capital proceeds' received by a shareholder for the disposal of their shares in the target company?

- Second, do the franking credits attaching to the special dividend pass to target shareholders?

A special dividend would be included in an Australian shareholder's assessable income. In addition, the dividend may be treated as part of the consideration for the sale of the shares and included in capital proceeds. The anti-overlap rule would generally mean the special dividend is taxed only once by reducing a capital gain made on the disposal by the amount of the special dividend (but not below zero—ie the special dividend would not result in, or increase, any capital loss).

Based on our review of class rulings published by the ATO in the previous nine years, we have identified the following trends:

- In all cases where the target funded the payment of the special dividend from its existing cash or debt reserves, the Commissioner ruled that the special dividend did not form part of capital proceeds.2

- In all cases where the bidder funded the payment of the special dividend, the Commissioner ruled that the special dividend did form part of capital proceeds.3

- In most cases, the declaration and payment of the special dividend was conditional on the scheme being effective or implemented.4

If a special dividend is paid (and forms part of capital proceeds) in a scrip-for-scrip deal, the dividend may affect the cost base of new shares acquired by a target shareholder. In particular, the cost base of the replacement shares will be permanently reduced by the portion of the cost base of the target shares that is reasonably attributable to the special dividend. On a subsequent disposal of those replacement shares, the amount of the special dividend would effectively be subject to tax again.5

For example, in the iiNet scheme, the Commissioner ruled that the special dividend paid by the company formed part of the capital proceeds received by shareholders for the disposal of their iiNet shares. The Commissioner required the iiNet shareholders to calculate the cost base of each new TPG share by reasonably attributing to it the cost base (or part of it, because only a partial scrip-for-scrip rollover was available) of the iiNet share for which it was exchanged. As a result, the cost base of the iiNet share was reduced by so much that it was reasonably attributable to the special dividend itself.6

Related payment

An entity will only be entitled to a gross-up and franking offset if it is a 'qualified person'—ie if they have satisfied the 'holding period rule' and the 'related payments rule'.

Based on the Commissioner's practice, if the special dividend reduces the amount of scheme consideration receivable by a shareholder for the disposal of their shares, the payment of the special dividend will likely constitute a 'related payment'.7

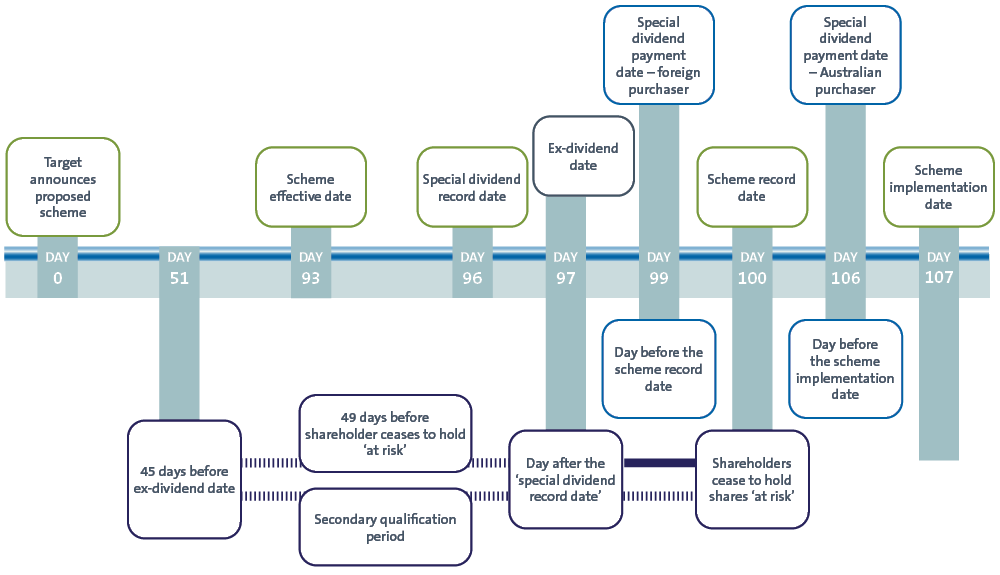

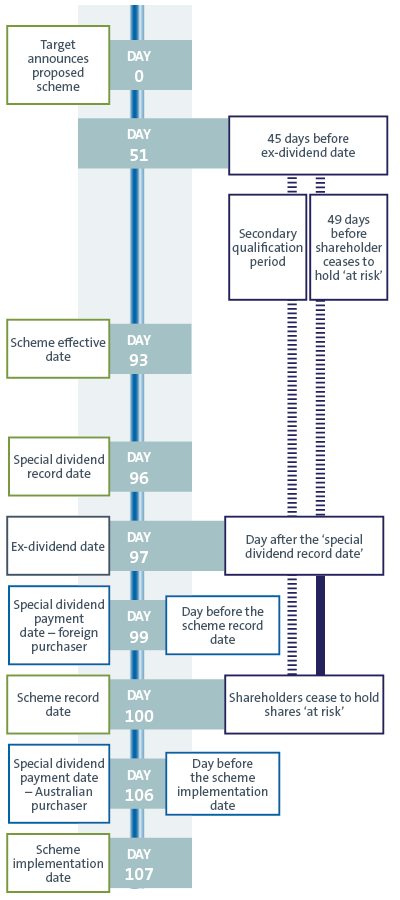

Based on our review of class rulings published by the ATO in the previous nine years, the Commissioner's practice is that a shareholder will be considered to no longer hold their shares ‘at risk’ on and from the 'Scheme Record Date'.8 This means that, where there is a related payment, in order for an entity to be a 'qualified person', the special dividend record date should be at least two days prior to the scheme record date.

'Exempting entity'

Where a company is an 'exempting entity', franking credits would generally (subject to certain limited exceptions) not be available to Australian resident shareholders.

In the context of a scheme, this issue will be particularly relevant where the bidder is foreign owned or controlled. In these circumstances, it will be critical for the special dividend to be paid prior to the time the target company becomes an 'exempting entity'. The ATO's historic approach has been that the exempting entity rules are not triggered (and therefore, franking credits not denied), even where the special dividend is paid after the scheme record date. The ATO is understood to be revisiting this position—for that reason, the special dividend payment date should be no later than the day before the scheme record date (see below), and early engagement with the ATO is essential.

Indicative timetable for a scheme

An indicative scheme timetable for the payment of a special dividend in the context of a scheme (taking into account the key dates described above) could be as follows:

Tax reform: new tax integrity rule

Whilst the ATO has issued class rulings in favour of the use of special dividends in M&A in recent times, it is an area to watch. The Government's proposed new integrity measure—which applies to special dividends funded by capital raising—could treat a special dividend paid in connection with a scheme as ‘unfrankable’ where the special dividend is funded directly or indirectly by a ‘capital raising’.

The key question in this context will be: how is the special dividend funded? Does the funding involve the issue of an ‘equity interest’ (for tax purposes) by any entity—eg the target, the bidder or anybody else? The ATO has previously flagged the possibility of applying the new integrity rule in this context.9

The proposed integrity measure is currently being reviewed by the Senate and may be subject to change. The Senate Economics Legislation Committee released a report indicating that while the Senate was supportive of the policy rationale behind the measure, it recommended the Government review the scope of the measure to ensure its targeted application.

ATO consultation: capital management

The ATO recently announced a public consultation process in relation to public listed companies undertaking certain capital management activities.

Relevantly, the ATO has asked for submissions on the utility of existing public guidance materials for dividends paid in connection with a scheme of arrangement, including whether there are other issues for which public guidance should be provided by the ATO.

Takeaway

Bidders and targets are looking for additional ways to unlock value for shareholders and to bridge bid-ask spreads in public transactions. Too often, we are observing transactions go cold, whether because of opportunistic bids being rebuffed by target boards, the increasing cost of debt or bidder boards/investment committees unable or unwilling to hit a target board's view on value. In these circumstances, special dividends and the value they can deliver in cash and franking credits may be the additional value you need.

Footnotes

-

Current as at 13 July 2023.

-

The only exception was in the case of Folkestone Limited (CR 2018/51) where, despite the target funding the special dividend, it was included in capital proceeds on the basis that the company was required to declare and pay the special dividend once the scheme was approved by shareholders.

-

See, for example, schemes involving Zenith Energy Limited (CR 2020/52) and AIRR Holdings Limited (CR 2019/74).

-

In a small number of cases the special dividend was not conditional and, in those cases, the special dividend did not form part of capital proceeds (see, for example, the scheme involving Asaleo Care Limited (CR 2021/47).

-

See, for example, CR 2015/71 in relation to the iiNet Limited scheme.

-

CR 2015/71 (paragraph 101).

-

See, for example, CR 2022/75 in relation to the Uniti Group Limited scheme.

-

See, for example, CR 2022/63 in relation to the Crestone Holdings Limited scheme.

-

See, for example, CR 2020/52 in relation to the Zenith Energy scheme.