Ground-breaking but complex reform 15 min read

From 1 July 2024, the Commercial and Industrial Property Tax Reform Act 2024 (Vic) (the Act) will provide for commercial and industrial property in Victoria to be subject to stamp duty for a final time when it is next sold or otherwise transacted. Ten years later, it will transition to the new annual Commercial and Industrial Property Tax (CIPT) imposed at the rate of 1% of the unimproved value of the land. The CIPT will be in addition to land tax, and properties that are not sold or transacted will remain outside the CIPT regime – which is intended to be a more economically efficient replacement for stamp duty that will assist Victorian businesses to set up in, expand and relocate to the most appropriate location.

On This Page

- Key takeaways

- How will land transition from stamp duty to CIPT?

- When does the transition from stamp duty to CIPT commence?

- What transactions result in land entering the CIPT regime?

- What land is subject to CIPT?

- Who is liable for CIPT?

- What is the rate of CIPT?

- Can CIPT be passed on to retail, residential and other lessees?

- How are subsequent transactions involving CIPT land treated?

- What happens if there is a subsequent change of use of land?

- What obligations apply to vendors of land?

- What is the transition loan program?

Key takeaways

- Current investors in industrial or commercial land, or landholders owning such land, who intend to retain their interest in land should not be affected by CIPT. Industrial or commercial land will only enter the CIPT regime if it is sold or transacted on or after 1 July 2024. However, minority investors may become subject to CIPT directly or indirectly if a majority interest in the land or its landholder is sold or transacted on or after 1 July 2024.

- A prospective purchaser of industrial or commercial land, or of a landholder owning such land, should consider executing the contract of sale before 1 July 2024. While stamp duty will be payable on the purchase both before and after that date, CIPT will only become payable by the owner of the land if the contract is executed on or after 1 July 2024. From 1 July 2024, all purchasers should ensure their due diligence procedures incorporate determining the CIPT status of land to be acquired (including by obtaining a property clearance certificate).

- From 1 July 2024, a vendor of industrial or commercial land must inform the purchaser in a section 32 vendor's statement whether or not land has entered the CIPT regime (and if so, when) and the Australian Valuation Property Classification Code (AVPCC) allocated to it. CIPT cannot be apportioned between vendor and purchaser where the contract sale price is less than $10 million.

- Lessors who acquire industrial and commercial land on or after 1 July 2024 cannot pass the cost of their CIPT liability on to residential or retail tenants, and so will need to factor that cost into the rent. However, the CIPT liability cost can be passed on to non-retail industrial and commercial tenants, provided the lease contains terms to this effect. Lessees under pre-1979 long-term non-Crown leases should be aware that they will have a statutory liability for CIPT if the lessor sells the leased land on or after 1 July 2024.

- The acquisition of an economic entitlement in relation to land or a landholder by a developer will not result in land becoming subject to the CIPT regime. However, the acquisition of an economic entitlement by a developer in relation to land that has entered the CIPT regime will remain subject to duty. The Victorian Government has stated it will consult further and introduce appropriate amendments to address this issue.

- Developers who acquire industrial or commercial land and redevelop it into (non-build-to-rent (BTR)) residential land will either pay duty on the acquisition (if they are a pre-1 July 2024 purchaser or the first post-1 July 2024 purchaser) or change of use duty (if they are a subsequent purchaser). Change of use duty will, however, not apply if the developer maintains the industrial or commercial use of the land for 10 calendar years after its acquisition before commencing the residential redevelopment.

- Prospective purchasers of industrial or commercial land valued up to $30 million who are interested in taking advantage of a government-facilitated 10-year loan to pay their stamp duty liability should be alert for further details of the transition loan program from the Treasury Corporation of Victoria (the Treasury Corporation).

How will land transition from stamp duty to CIPT?

The CIPT regime will replace transfer duty and landholder duty on commercial and industrial properties in Victoria sold or transacted on or after 1 July 2024.

Land enters the CIPT regime if, broadly, a post-1 July 2024 contract of sale or other transaction document is executed involving at least a 50% interest in the land, a positive stamp duty liability, and land with a qualifying commercial or industrial use at settlement. In such circumstances:

- a final stamp duty liability will be incurred on the land and paid by the purchaser;

- taxpayers can pay the final stamp duty amount upfront or, if eligible, in annual instalments over a 10-year transition period commencing on the date the land enters the CIPT regime, using a transition loan offered by the Treasury Corporation;

- CIPT will then become payable by the owner of the land for each year commencing after a 10-year transition period, if the land continues to have a qualifying use as at midnight on the preceding 31 December; and

- subsequent transactions involving land that has entered the CIPT regime will generally be exempt from transfer duty and landholder duty, if the land continues to have a qualifying use.

When does the transition from stamp duty to CIPT commence?

The CIPT regime will only apply to commercial and industrial property the subject of transactions with both a contract and settlement date on or after 1 July 2024. The CIPT regime will not apply to land the subject of a dutiable transaction liable to transfer duty, or a relevant acquisition in a landholder liable to landholder duty, if the transaction or acquisition occurs under an agreement or arrangement that was entered into before 1 July 2024.

This means that if a contract is entered into before 1 July 2024, the purchaser will only be liable to stamp duty and the land will not transition to the CIPT regime after the 10-year transition period, even if settlement occurs on or after 1 July 2024. In contrast, if a contract is entered into on or after 1 July 2024, the purchaser will be liable for stamp duty and the land will transition to the CIPT regime after the 10-year transition period. As such, a purchaser who does not wish to pay both stamp duty and CIPT should seek to sign the contract by 30 June 2024.

Industrial and commercial property that is not the subject of any transaction on or after 1 July 2024 will not transition to the CIPT regime.

What transactions result in land entering the CIPT regime?

Industrial and commercial property will enter the CIPT regime if an 'entry transaction' occurs. Broadly, if an agreement or arrangement for the acquisition of at least a 50% interest in the land (either direct or indirect, and either alone or when aggregated with certain other interests in the land) is entered into on or after 1 July 2024, that gives rise to a transfer duty or landholder duty liability.

This means that transactions eligible for an exemption from stamp duty under the Duties Act 2000 (Vic) will not enter the CIPT regime (eg transfers to and from deceased estates, between spouses and partners, and purchases by charities and friendly associations). However, the Explanatory Memorandum to the Act makes clear that relevant acquisitions of interests in a public landholder that are merely eligible for a concessional rate of duty may still be considered to be an entry transaction.

The Act also excludes the following complex transactions from being an entry transaction:

- the granting, transfer or assignment of a lease over land for which consideration other than rent is provided (if no such consideration is provided, the transaction is not dutiable in the first place);

- dutiable transactions relating to, or relevant acquisitions arising from, the acquisition of economic entitlements in land or private landholders; and

- transactions that qualify for a duty concession under the corporate consolidation or reconstruction rules (defined as 'eligible transactions' in s250A of the Duties Act).

Property will also enter the CIPT regime if:

- land that has entered the CIPT regime is consolidated with land that has not entered the CIPT regime, and 50% or more by area of the consolidated property is subject to the CIPT; and

- land that has already entered the CIPT regime is subdivided to create new lots. The new lots will be taken to have entered the CIPT regime when their parent lot previously did.

What land is subject to CIPT?

Land can only enter into and remain within the CIPT regime if it has a 'qualifying use' (broadly speaking, a commercial or industrial use).

Land has a qualifying use if:

- it is allocated a certain AVPCC; or

- it is used solely or primarily for eligible student accommodation.

AVPCCs are allocated to land as part of the valuation process under the Valuation of Land Act 1960 (Vic). Only land allocated AVPCCs within the ranges 200–499 or 600–699 will have a qualifying use and be subject to the CIPT regime (ie land within the commercial, industrial, extractive industries, industrial infrastructure and utilities classifications).

Land allocated AVPCCs within and outside those ranges (ie mixed-use land) will have a qualifying use and be subject to the CIPT regime if it is used solely or primarily for a use within the range of qualifying uses. This sole or primary use test will apply to determine the treatment of mixed-use land; there will be no apportionment for such land (ie land is either wholly in or wholly out of the CIPT regime).

Land that is not taxable land for land tax purposes (ie exempt land for land tax purposes) will not be subject to CIPT.

This means that the following categories of land are excluded from the CIPT regime:

- land used for residential purposes (other than BTR land);

- land used for primary production, community services, sport, heritage or culture purposes;

- national parks, conservation areas, forest reserves and natural water reserves; and

- mixed-use land that is primarily used for non-commercial or non-industrial uses.

The CIPT regime is intended to apply to BTR land, but it is not immediately apparent from the current AVPCCs that operational BTR sites would fall within the qualifying use ranges in the first place. An amendment to the Act may be required to specifically include BTR land (similar to the express inclusion of eligible student accommodation) if such land is intended to be within the CIPT regime.

Interestingly, where land that has entered the CIPT regime is consolidated with land that has not entered it, and 50% or more by area of the consolidated property is not subject to the CIPT, the consolidated property ceases to be subject to the CIPT.

Who is liable for CIPT?

The owner of the land that has entered the CIPT regime will generally be liable to pay the annual CIPT. The owner liable to pay the CIPT is the same as the owner of the land for land tax purposes, subject to some exceptions.

These are that holders of beneficial interests in trusts are not deemed to be owners, while lessees under non-Crown leases granted before 1979 are deemed to be owners, with the CIPT liability apportioned between such long-term lessees and the lessor. Such long-term lessees may thus have a statutory liability for CIPT purely because the lessor sells the freehold land on or after 1 July 2024.

The Act also gives the Commissioner of State Revenue (the Commissioner) power to recover unpaid CIPT by garnishee notice from the occupier, lessee or mortgagee of a property if the owner is in default. Unless the occupier or lessee is a related party of the owner, the amount recoverable from them is limited to rent as it becomes payable.

What is the rate of CIPT?

CIPT will generally apply at a flat per annum rate of 1% of the land's site value (ie the unimproved market value) as at 31 December immediately preceding the year, with no tax-free threshold. This is the same land value upon which land tax is imposed, but a different rate.

For land that is eligible for a BTR land tax benefit under the Land Tax Act 2005 (Vic), a concessional rate of 0.5% per annum will apply.

The Act does not contemplate a foreign absentee owner surcharge like that applying to foreign owners of commercial and industrial property for the purposes of land tax.

CIPT will be imposed in addition to, and not in replacement of, other taxes, including land tax, windfall gains tax, local government rates and charges, and the fire services property levy.

Can CIPT be passed on to retail, residential and other lessees?

Landlords will not be permitted to pass on the CIPT to retail and residential tenants.

To this end, the Act amends s50 of the Retail Leases Act 2003 (Vic) to prohibit CIPT from being passed on to tenants under a retail premises lease, consistent with the treatment already applied to land tax.

Passing on CIPT to renters under a residential rental agreement will also be prohibited by s30 of the Act itself, consistent with the treatment already applied to land tax under s99 of the Land Tax Act. Given that CIPT only applies to land with a qualifying use (ie industrial and commercial land), this prohibition will be most relevant to BTR tenants.

However, no such prohibition applies to other tenants, such as non-retail commercial or industrial tenants. Nor does either prohibition prevent a retail or residential landlord from setting the rent so as to recover the cost of its CIPT liability.

How are subsequent transactions involving CIPT land treated?

Once land has entered the CIPT regime, provided the land continues to have a qualifying use:

- subsequent dutiable transactions involving the land will generally be exempt from transfer duty; and

- subsequent relevant acquisitions in the landholder that owns the land will benefit from a concessional reduction in landholder duty, due to the unencumbered market value of the land being excluded from the underlying land of the landholder upon which landholder duty is calculated.

If the entry transaction involved the acquisition of a 100% interest in the land, the transfer duty exemption and landholder duty concession will be immediately available for subsequent transactions involving the CIPT land, meaning that no transfer duty or landholder duty will be payable for the land on those transactions. For example, where a 100% interest in land is purchased in 2025, resulting in the land entering the CIPT regime, and then sold in 2030, no duty will be payable on the 2030 sale.

If the entry transaction involved a fractional interest of less than 100% in the land (eg the purchase of a 60% interest in land), the transfer duty exemption and the landholder duty concession will only be available for that interest in the land. The transfer duty exemption and landholder duty concession will not be available for the other interest in the land (eg the remaining 40% interest) if fewer than three years have passed since the entry transaction.

Once three years has passed, the transfer duty exemption and the landholder duty concession will apply to the entirety of the land.

Importantly, the exemption and concession do not apply in relation to dutiable transactions or relevant acquisitions excluded from being entry transactions (eg acquisition of economic entitlements) or other complex transactions (eg transfers of dutiable fixtures and goods used or held in connection with land). The Victorian Government has stated that it intends to exempt such transactions with appropriate amendments later this year.1

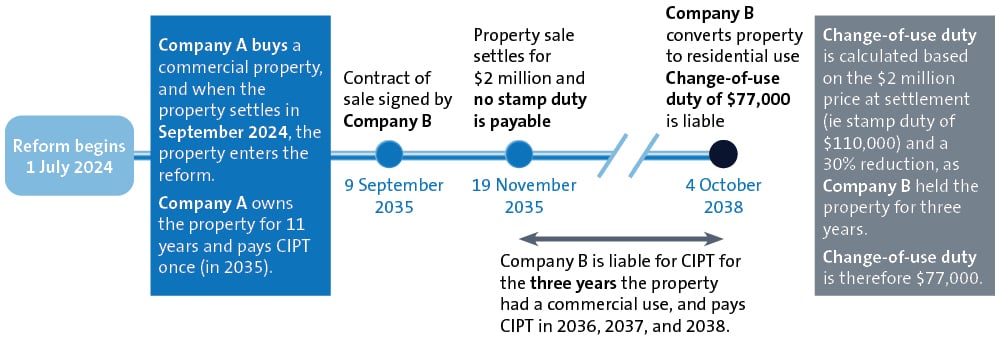

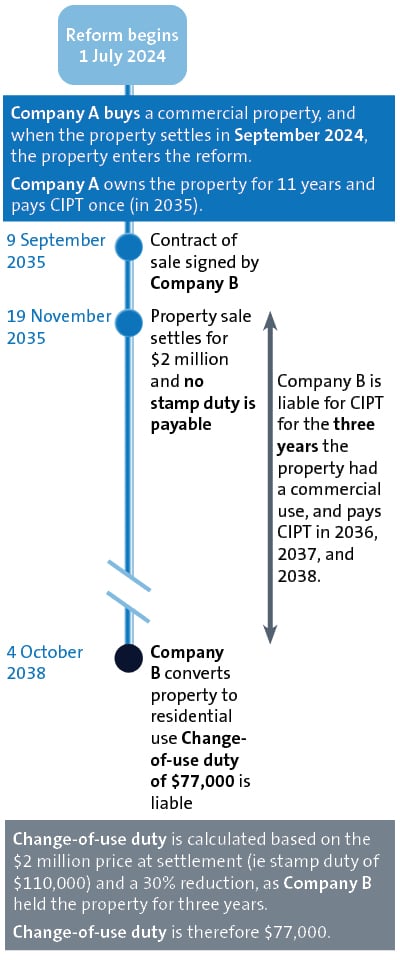

What happens if there is a subsequent change of use of land?

If there is a change of the use of land that has entered the CIPT regime to a non-qualifying use, the owner of the land will no longer be subject to CIPT on the land. If the owner subsequently sells the land, transfer duty will be payable by the purchaser. (In contrast, if there had been no change in use of the land, the owner would have continued to be subject to CIPT, but no transfer duty would have been payable by the subsequent purchaser, who would become subject to CIPT as the new owner.)

However, once land has entered the CIPT regime as a result of the first post-1 July 2024 transaction involving the land, and is subsequently onsold to a second post-1 July 2024 purchaser (who will not be liable for transfer duty on that sale if there has been no change to the qualifying use of the land), but that second purchaser subsequently converts the land to a non-qualifying use, a 'change of use duty' will apply. This is because both transfer duty and the CIPT would otherwise be avoided by the subsequent purchaser.

The change of use duty imposed will be the ad valorem transfer duty that would have been payable when the land was purchased by the second post-1 July 2024 purchaser, reduced by 10% for each calendar year that has elapsed following the second post-1 July 2024 purchaser's acquisition. If a property ceases to be used for a qualifying purpose 10 years or more after the second post-1 July 2024 purchaser's acquisition of the interest in the property, no change of use duty will apply, because the policy intention of the reform is that any purchaser should bear liability for the CIPT for 10 years, or a proportionate amount of change of use duty.

If and when a property converts to a qualifying use after having previously converted to a non-qualifying use, CIPT will be payable by the same owner and there will be no refund for the change-of-use duty.

Similarly, if landholder duty was calculated under the CIPT regime concession and the use of the CIPT land changes to a non-qualifying use, the Commissioner must reassess additional landholder duty payable on the earlier relevant acquisition. Consistent with the position for transfer duty, this will be the landholder duty that would have been payable for the CIPT land, with a 10% discount for each calendar year that has elapsed since the date of the relevant acquisition.

Owners of land that has entered the CIPT regime have an obligation to notify the Commissioner, through the Victorian State Revenue Office, within 30 days of any change of use of the property.

The following diagram contains an example of change of use duty:2

What obligations apply to vendors of land?

Statements given by vendors to purchasers under s32 of the Sale of Land Act 1962 (Vic) must state whether or not the land has entered the CIPT regime, the AVPCC allocated to the land and when the property entered the CIPT regime.

Similarly, property clearance certificates issued by the Commissioner under s95AA of the Taxation Administration Act 1997 (Vic) will now include information regarding whether land has entered the CIPT regime, when it entered the CIPT regime, when it will become subject to CIPT and the amount of any outstanding CIPT payable.

Where the sale price under a contract of sale of land is less than $10 million, liability for CIPT cannot be apportioned between the vendor and purchaser. Vendors will need to recover any CIPT liability indirectly through the purchase price.

What is the transition loan program?

Certain purchasers will have the choice of paying the final stamp duty liability for a property upfront, using their own funds (ie the standard approach under the current stamp duty regime), or by accessing a government-facilitated transition loan.

The loan proceeds must be repaid with interest by the purchaser in annual instalments over a 10-year period. The purpose of the transition loan is to help smooth the transition to CIPT, and allow taxpayers who opt for the loan to effectively transition to annual payments from the time of purchase (ie loan repayments for the first 10 years, and thereafter CIPT payments).

The Act provides that transition loans will be provided by the Treasury Corporation and secured by a first-ranking statutory charge over the land for any amounts owing under the transition loan. The transition loan will be registered on title, prioritised ahead of all other encumbrances and confer on the Treasury Corporation a statutory right of sale over the land in the event of default.

The Treasurer will be able to determine any matter regarding the operation of the transition loan program by written notice given to the Treasury Corporation and published in the Government Gazette (including loan eligibility criteria, and terms and conditions). Otherwise, the Treasury Corporation will determine any other matter regarding the operation of the program.

The Victorian Department of Treasury and Finance has published a Fact Sheet in relation to the transition loan program.3 It sets out the following key eligibility criteria:

- the property has a value up to $30 million (equivalent to $1.93 million in transfer duty);

- the applicant is an Australian business entity or Australian citizen/permanent resident; and

- the applicant has received finance pre-approval for the property from an authorised deposit-taking institution or registered financial corporation holding an Australian credit licence.

The Fact Sheet also indicates that the loan terms and conditions will be non-negotiable, and include the following key items:4

- interest payable at a fixed commercial rate, being the Treasury Corporation's base rate plus a margin (with an illustrative rate of 7.12%);

- a prohibition on a transition loan being novated, or transferred to a third party or subsequent purchaser; and

- an obligation for the borrower to repay the outstanding balance of the loan:

- before the property can be sold and transferred;

- if the property changes to a non-qualifying use;

- on the occurrence of prohibited activities or adverse findings; and

- in the event of failure to make a payment when due, insolvency/bankruptcy or breach of law.

While there is a prohibition on landlords passing on CIPT to residential or retail tenants, there does not appear to be any prohibition on landlords passing on loan repayments (either by way of reimbursement or recovery as part of rent).

If you wish to discuss the issues raised in this Insight, and/or require assistance, please contact any of the people below.

Footnotes

-

Victoria, Parliamentary Debates, Legislative Council, 14 May 2024, 1557 (Jaclyn Symes, Attorney-General).

-

Victorian Government, Commercial and Industrial Property Tax Reform Information Sheet, 9.

-

Victorian Government, Commercial and Industrial Property Tax Reform: Fact Sheet – Transition Loan Key Design Elements, 3.

-

Ibid., 4–5.