Updates to the regime 9 min read

Vietnam's merger control regime captures a wide range of onshore and offshore transactions, due to extensive notification thresholds. This has led to a significant increase in filings to the Vietnamese competition authority in recent years, including for transactions with limited impact on the Vietnamese market. In practice, the filing process can be lengthy and complicated, which may affect the overall transaction timeline. Further reform is now underway, including an increase in the filing thresholds, as the Government seeks to narrow the scope of notifiable transactions and reduce the regulatory burden on deals that raise limited competition concerns in Vietnam.

In this updated Vietnam merger control guide, we provide a consolidated overview of the regime's key aspects, including filing requirements, the review process, recent practice and the latest reform developments.

What transactions are captured

- Vietnam’s merger control regime generally captures 'economic concentrations', including foreign-to-foreign transactions conducted outside Vietnam. 'Economic concentrations' include mergers, consolidations, acquisitions and joint ventures1, each as defined in the law. The regime also captures 'other types of economic concentration provided by law', which have not been specifically identified so far. An economic concentration is generally notifiable if it satisfies any of the merger filing thresholds discussed below.

- There is no specific exception or simplified review process for intra-group 'economic concentrations' for internal restructuring purposes, as in other jurisdictions. In fact, there are public records of intra-group restructurings being filed and cleared. Merger control filing for internal restructurings should be considered on a case-by-case basis. Recently, review timing for such transactions appears to have been shortened, although no official fast-track process has been introduced.

Concept of 'control'

- Acquisition of shares or assets by investors (including foreign strategic or financial/private equity investors) is the most common form of economic concentration in practice.

- The Vietnam merger control regime only captures acquisitions that confer 'control' in the target company to the acquirer.

- 'Control' is considered to be conferred where any of the following applies:

- ownership of more than 50% of the charter capital or voting shares, or assets of all or one business line/sector of the target; or

- having the right to:

- directly or indirectly appoint or dismiss a majority or all members of the board of management, chairperson of the members’ council, director or general director of the target;

- amend the charter of the target; or

- decide important matters regarding the target's business operations, such as business lines, geographical areas and forms of business, adjustment to the scale of business; and the form and method of raising, allocating and utilising business capital.

- 'Negative control' (such as veto rights regarding important corporate decisions) is not expressly captured by the above 'control' test, and the Vietnam competition authority has informally confirmed this.

Merger filing thresholds and calculations

Vietnamese competition law captures economic concentrations 'causing, or capable of causing, a competition-restraining impact in the Vietnamese market'. This local impact should be assessed on a case-by-case basis for relevant economic concentrations based on, among other things, the parties' local presence in Vietnam.

An economic concentration is generally notifiable if any merger filing threshold is met by any party to the transaction,2 irrespective of whether there is any overlap between the parties.

The previous filing thresholds are low relative to the size of the Vietnamese market, resulting in a high volume of filings to the Vietnam Competition Commission (the VCC). Higher thresholds have been introduced on a pilot basis from 1 July 2026 to 28 February 2027, while the Government is amending the implementing decree to formally adopt new filing thresholds, although it remains unclear how they will ultimately be reflected.

|

Threshold |

Previous thresholds (applicable until 30 June 2026) |

Current thresholds (applicable from 1 July 2026 to 28 February 2027) |

|---|---|---|

|

Total assets or total turnover Total assets or total sales turnover/input purchase turnover in the Vietnamese market of any party or group of affiliated enterprises of such party in the previous financial year |

VND3 trillion (c. USD114 million) or more |

VND6 trillion (c. USD228 million) or more |

|

Transaction value Transaction value (for onshore transactions conducted in Vietnam only) |

VND1 trillion (c. USD38 million) or more |

VND2 trillion (c. USD76 million) or more |

|

Combined market share Combined market share of all parties to the economic concentration in the relevant market in the previous financial year |

20% or more |

20% or more (unchanged) |

'Total assets' and 'total turnover' thresholds

- In practice, 'total assets' and 'total turnover' are the most common thresholds to trigger the merger filing requirement in Vietnam.

- Any party satisfying the above 'total assets' or 'total turnover' thresholds in Vietnam should be cautious, as its transactions (in Vietnam or offshore) may trigger the merger filing requirement on the basis that that party alone satisfies the relevant filing threshold.

- Some key rules on calculation of the 'total assets' and 'total turnover' thresholds are as follows:

- These thresholds apply on an individual basis to any party to the transaction (eg the seller, the target company or the acquirer in an acquisition transaction), and not the combined 'total assets' or 'total turnover' of all parties.

- These thresholds must be calculated on a consolidated basis regarding the relevant party's 'group of affiliated enterprises', which includes entities that the relevant party controls, is controlled by and is under common control with, according to the 'control' test described above.

- These thresholds cover assets/turnover across all business sectors/markets where the relevant party is active in Vietnam (and not only the market(s) relevant to the proposed transaction).

- These thresholds also cover assets and turnover in Vietnam of offshore entities within the relevant group, even where they do not have a local presence. Eg cross-border sales into Vietnam via local distributors are also captured.

'Combined market share' threshold

- The 'combined market share' threshold of 20% or more is calculated only in respect of the market(s) relevant to the proposed transaction (and not across all markets where the parties have a presence in Vietnam).

- The relevant market is determined based on the relevant product market and the relevant geographical market. Complex technical analysis of the parties' business operations would be required to determine the relevant market. Often, there may be several relevant markets that need to be considered.

- If a party is part of a group of affiliated enterprises, its market share will be determined on a consolidated group basis, based on the total turnover or volume of the group companies in the relevant market, less the intra-group generated turnover or volume.

Merger filing and review process

Responsible authority

The VCC is responsible for merger filing reviews.

Filing responsibility

All parties to a notifiable economic concentration are jointly responsible for the merger control filing in Vietnam.

Filing fees

No filing fee is payable for merger control filings in Vietnam.

Filing documentation

- The merger filing submission comprises numerous documents, which can take considerable time to prepare. These include the notification form, draft transaction agreement or memorandum of understanding, the parties' corporate documents, lists of subsidiaries/affiliates and products traded, a market share report and competition impact assessment report. Many of these documents must be legalised overseas and translated into Vietnamese. Accordingly, the merger filing process should be assessed and commenced as early as possible, to avoid delays in the overall transaction timeline.

- Filings are submitted through the VCC's online portal, and colour-scanned copies of filing documentation are generally sufficient. However, it may request hard copies during the review process.

- A market share report and competition impact assessment report are required in all submissions, even where there is no overlap between the parties. These reports must address the relevant market(s), the parties' market shares and the transaction's potential competition impact in the Vietnamese market.

- Parties can request that their merger filing submission be kept confidential by including this in the filing to the authority.

- A transaction with multiple steps or phases can be filed in a single consolidated submission, provided the steps involve the same parties, are linked and will be completed within a short period.

Pre-completion clearance requirement

Parties to a notifiable economic concentration must obtain a merger control clearance before they carry out an economic concentration.

Merger review process

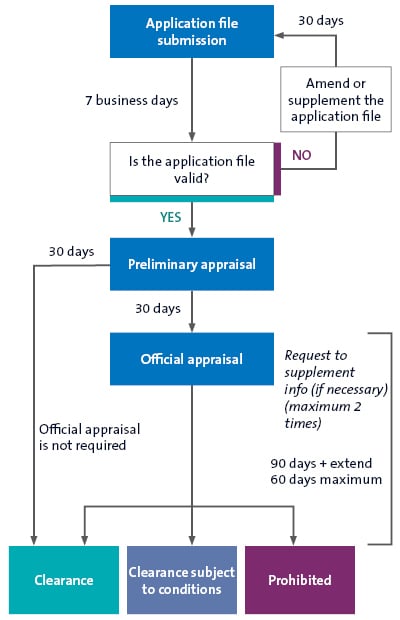

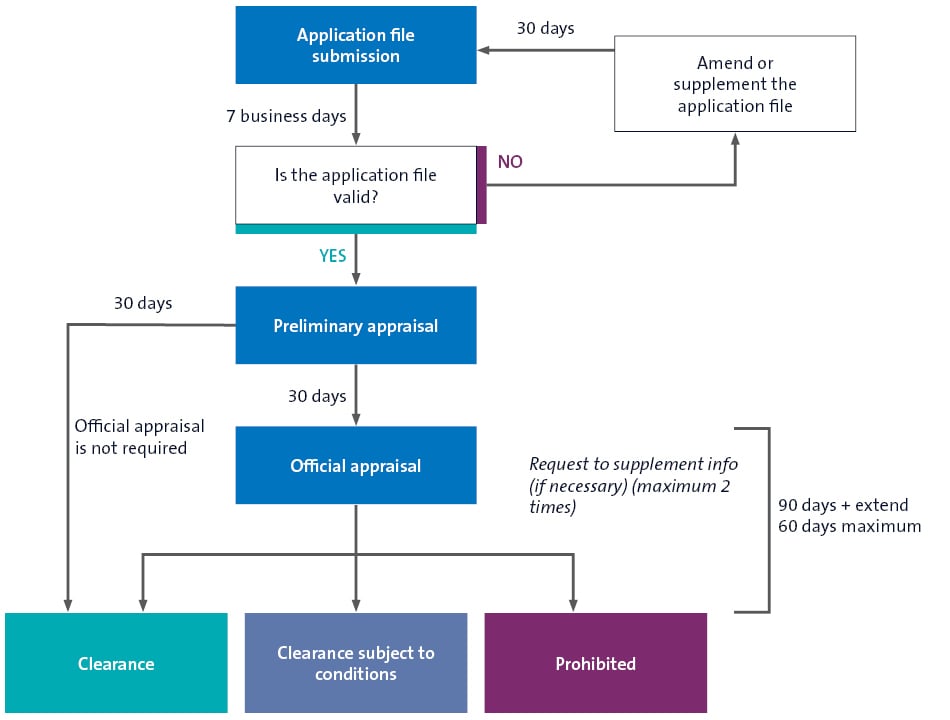

- Vietnamese law prescribes a two-phase merger review process, comprising:

- the preliminary appraisal; and

- the official appraisal.

- To date, most filings are cleared at the preliminary appraisal phase, with only a small number proceeding to official appraisal.

The two-phase merger review process is illustrated below:

Preliminary appraisal phase

- Simple or no-issue filings are likely cleared at the preliminary appraisal phase if they satisfy the 'safe harbours' test, which is based on the combined market share of the parties and/or the Herfindahl-Hirschman Index. Eg a transaction will likely be cleared at this phase if the combined market share in the relevant market is less than 20%.

- A transaction is deemed to be cleared if the competition authority has not issued any written objection after 30 days from its receipt of a complete and valid merger filing dossier. In practice, so far, the VCC has always issued written official clearances.

- The preliminary appraisal phase usually takes at least three to four months, including preparation of filing documents. The VCC is considering a fast-track review process for no-issue cases, though it remains unclear when this will be introduced.

Official appraisal phase

More complex transactions are likely to proceed to the official appraisal phase (which may take up to, approximately, six months). In this phase, the authority assesses the competition-restraining impact and any positive economic impacts of the transaction to determine whether clearance should be granted.

The official appraisal phase may result in one of the three outcomes below:

- Unconditional clearance: the transaction is cleared and the parties can proceed with it without any conditions.

- Conditional clearance: the transaction is cleared subject to conditions or measures to remedy any anti-competitive effects. These conditions usually apply to the target post completion and are tailored on a case-by-case basis. Common conditions include periodic reporting and reporting on request on topics such as pricing formulae or price increases. Less common conditions include ensuring greater transparency for partners and customers, adoption of advanced technology, or product quality improvements.

- Prohibited merger: the transaction is prohibited on the basis that it 'causes or is capable of causing a significant competition-restraining impact in the Vietnamese market'. This is determined based on various factors, such as the parties' combined market share, the extent of concentration in the relevant market and the proposed transaction's impact on the relevant market.

No transaction has been reported to be blocked by the competition authority since the new merger control regime was adopted in May 2020.

Penalties, remedies and enforcement

Administrative sanctions and other remedies may be imposed for breaches of merger control regulations, as set out below.

To date, there has been very limited issuing of administrative fines for breaches of merger control filing obligations.

|

Breach |

Responsible parties |

Administrative fines |

Additional remedies |

|---|---|---|---|

|

Failure to file |

Each party to the transaction |

Up to VND2 billion (c. USD76,000) — capped at 5% of the total revenue in the relevant market in the previous financial year |

N/A |

|

Gun-jumping or pre-clearance closing |

Each party to the transaction |

Up to VND2 billion (c. USD76,000) — capped at 5% of the total revenue in the relevant market in the previous financial year |

N/A |

|

Prohibited transactions |

Depending on the form of the prohibited economic concentration |

1% to 5% of the total revenue in the relevant market in the previous financial year |

Demerger or split of the merged/consolidated entity, sale of the acquired interest, or compulsory control by the state over the prices for buying/selling goods/services, or other conditions |

The above penalties are calculated on 'total revenue in the relevant market'. There is no specific guidance on application, but this is likely to be interpreted as total revenue in the relevant markets in Vietnam subject to the proposed transaction (rather than across all markets in which the parties operate).

Footnotes

-

Based on the definition under Vietnamese law, a ‘joint venture’ requires the joint venture parties to contribute a portion of their lawful assets, rights, obligations and interests in order to form a new joint venture enterprise. Therefore, it seems that unincorporated joint ventures would not be captured by the Vietnam merger control regime.

-

Different thresholds apply in the case of economic concentrations involving a credit institution, an insurance company or a securities company.