Filing numbers back up, driven by competing claims and emerging areas of risk 5 min read

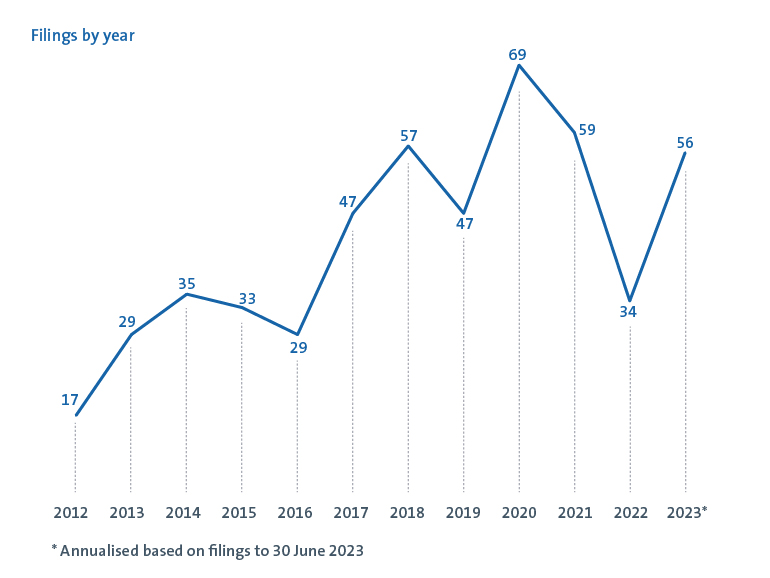

Class action filings in 2023 are on pace to significantly outstrip the number of claims filed last year, reverting to the trend of elevated filings seen over recent record setting years.

In this interim report we provide a high-level overview of the types of claims and some of the factors that have contributed to the growth in filings this year. A more detailed and holistic picture of class action trends and developments will be provided in our annual Class Action Risk report, which will be published in early 2024.

Filings on the rise

The key takeaway is that filings in the first half of the year were significantly higher than the equivalent period last year. There were 28 class actions filed to 30 June 2023, which is double the 14 class actions filed over the equivalent period in 2022, signalling a projected return to the all-time, high filing rates of 2017-21.

The increase in filings has been fuelled by a rise in competing class actions and the first significant wave of cyber class actions, following several high-profile data breach incidents. At the halfway mark of the year:

- 12 of the filings were competing class actions (comprising claims commenced on a 'copycat' basis after a similar class action was already on foot); and

- 5 of the filings were claims arising from data breach incidents.

Over the equivalent period last year, there were only two competing class actions and no data breach proceedings.

While the majority of class actions have continued to be filed in the Federal Court, filings in the Supreme Court of Victoria have continued to gain momentum, accounting for 40% of filings for the year to date (up from 28% over the course of 2022), as plaintiff lawyers continue to pursue the group costs orders (ie contingency fees) which are, at present, uniquely available in Victoria.

Broad base of claims with emerging areas of risk

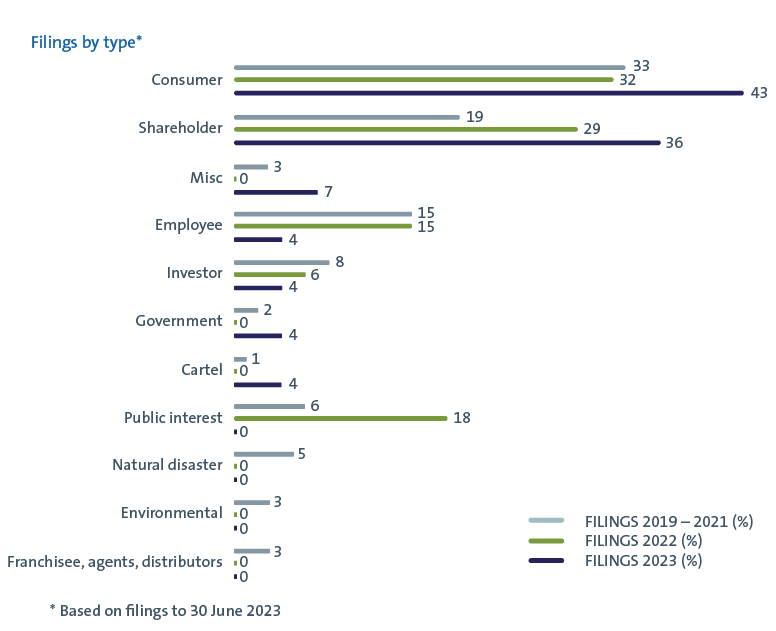

Consumer and shareholder class actions continue to dominate filings, with over 75% of all class actions for the year concentrated on these two forms of claims.

In building on a recent trend, the majority of consumer filings have targeted automakers. However, this year has also seen the emergence of a new type of consumer claim brought on behalf of people impacted by data breach incidents.

While most of the shareholder class actions have focused on earnings guidance disclosures (the conventional catalyst for these claims), there continues to be a growing trend of shareholder claims based on disclosures concerning alleged inadequate systems and controls, including in connection with the management of cybersecurity risks.

The rate of employment claims has continued to dwindle, coming off the highs of recent years. This development is likely the result of recent law reform and two High Court decisions which appear to have dealt a fatal blow to certain forms of employment claims.

It also appears that we are now working through the tail-end of COVID-19-related claims. There was one filing against the Government in relation to vaccine-related injuries, and another filing against a nursing home brought by families of residents who contracted the virus.

Similar risk across a range of sectors

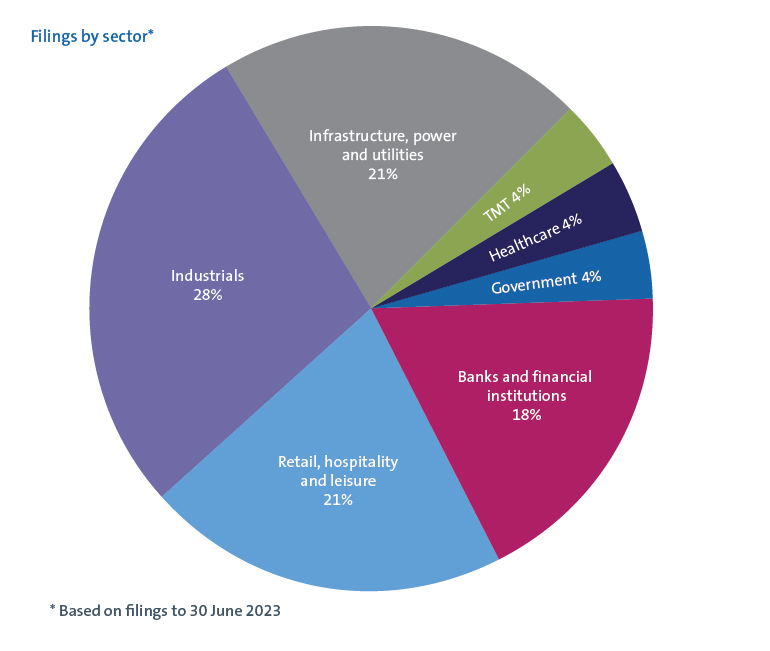

So far we've seen a similar situation unfold to last year, with a number of sectors facing a broadly equivalent class action risk and no sector facing a disproportionately greater risk than others. The sectors that have been under the most pressure through the first half of the year are:

- Industrials

- Infrastructure, power and utilities

- Retail, hospitality and leisure

- Banks and financial institutions.

However, it is apparent that filing levels across these sectors have been driven by the high rate of competing class actions rather than a range of different risks specific to each sector. For example, four of the six class actions in the infrastructure, power and utilities sector are competing claims brought against the same company and the issue of multiplicity impacts six of the eight class actions in the industrials sector involving automakers. Interestingly, while claims against banks and financial institutions represent 18% of filings, in a continuation of the position throughout last year, none of those filings involve claims brought against any of the banks.

What does it all mean for class action risk?

Class action risk is continuing to evolve, with promoters pursuing a wide-ranging spectrum of claims branching into green fields. Most significantly, while cybersecurity and data breach class actions have long loomed large on the horizon as potential areas of risk, through the first half of the year we have seen the first serious foray into this arena in the form of several consumer and shareholder claims.

Throughout the remainder of the year there are likely to be a number of judgments and developments that impact class action risk, including in relation to the important issue of litigation funding. We will provide our insights on these issues in our annual class action review, which will be published in early 2024.

If you would like to discuss how these trends and risks impact you, please contact the Allens class actions team below.