A surplus of hydrogen strategies 20 min read

With the world's first hydrogen cargo being shipped from Victoria in January 2022, production of hydrogen at scale in Australia seems closer than ever. However, developing a successful hydrogen industry requires appropriate policies, regulations, and incentives at both national and state levels. All Australian state and territory governments, as well as the federal government, have now released strategies for the development of a hydrogen industry – and many are providing significant financial incentives to kick-start it.

However, with more than a dozen different hydrogen policy statements and strategies now in force, it can be challenging for stakeholders and industry participants to work out what it all means, let alone identify the best policy settings for their projects. There is clear frustration at the lack of coordination by states and territories, particularly when a nationally consistent regulatory framework is a goal of the National Hydrogen Strategy (National Strategy).

In this Insight, we compare and contrast the different approaches taken in each jurisdiction around Australia.

On This Page

Key takeaways

- Australian federal, state and territory governments are all highly supportive of developing a hydrogen industry, with various strategies and plans in place. However, the sheer number of policies and lack of coordination between governments has the potential to create confusion and unnecessary complexity for stakeholders.

- While all states and territories acknowledge that some level of regulatory change is required to facilitate hydrogen production, few regulatory reforms have been made to date. Where progress has been made, the current approach appears to be one of states 'going it alone', meaning that the regulatory requirements for a hydrogen project may end up being different in each state and territory.

- The development of Renewable Energy Zones (REZs) or strategic development precincts will be important for renewable hydrogen production. New South Wales, Victoria, Queensland and Tasmania specifically link REZ development with hydrogen production, while Western Australia and the Northern Territory include hydrogen in plans for strategic development precincts.

- The financial incentives in each state and territory will influence the attractiveness of one jurisdiction over another as a place for hydrogen investment. However, the wide variance between incentives makes it difficult to compare and assess which jurisdictions are most attractive.

- Whereas some states, like NSW and ACT, have committed to pursuing 'green' hydrogen only, other states and territories only refer to 'renewable hydrogen' (it is unclear whether this includes 'blue' hydrogen). Meanwhile, the Australian Government's strategy explicitly includes 'blue' hydrogen under the umbrella of 'renewable hydrogen' and expresses support for developing carbon capture and storage solutions.

- Aside from the ACT, all states and territories have ambitions to be exporters of hydrogen to Asian markets, primarily Japan, South Korea and China. This is on top of hydrogen production for domestic use, particularly for transport and blending in gas networks.

Who in your organisation needs to know about this?

All entities considering developing or investing in hydrogen projects in Australia should be aware of the differences in the policies adopted by the Australian and state and territory governments and understand the implications for their projects.

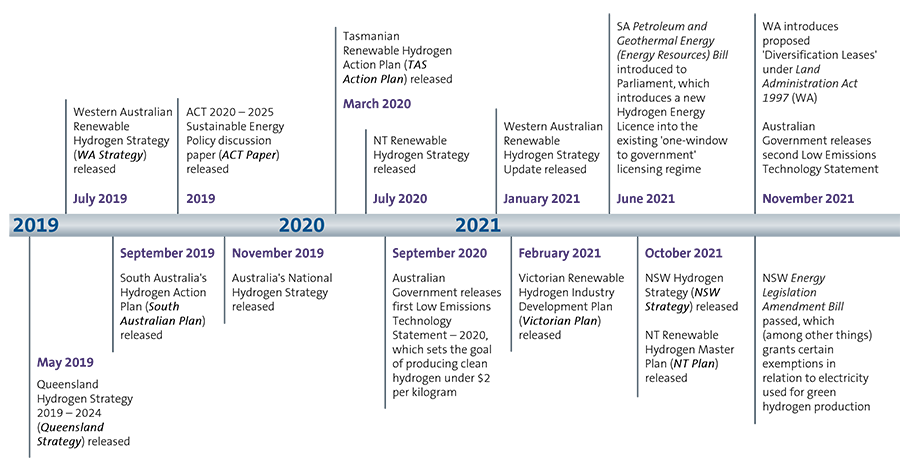

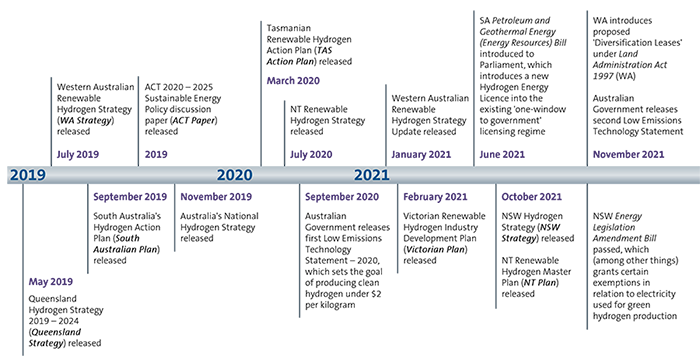

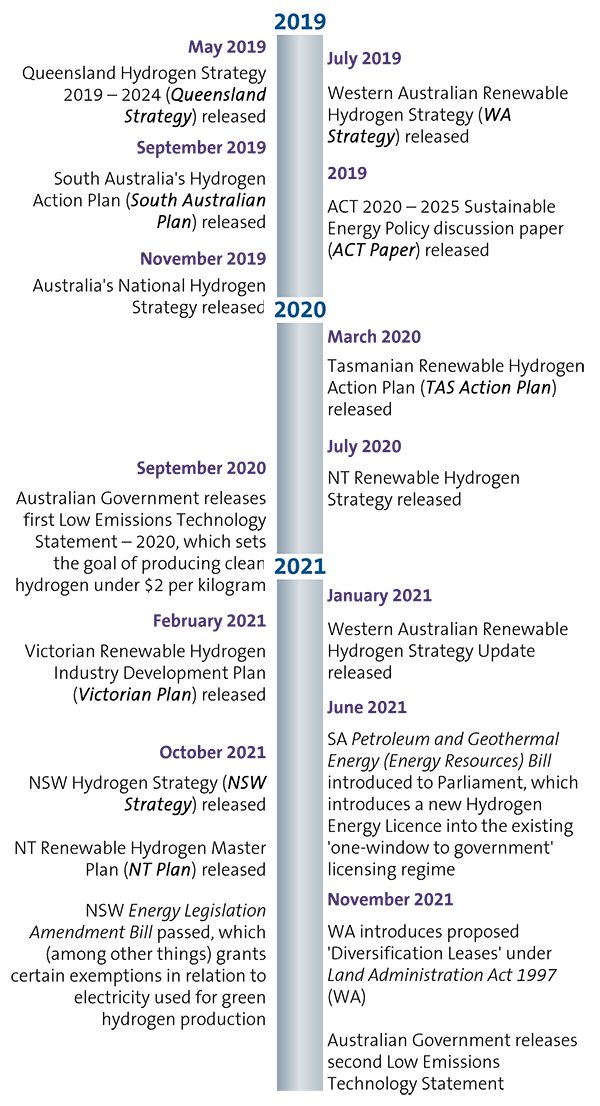

Development of hydrogen strategies

Timeframe for strategies

In line with the National Strategy, most state and territory hydrogen strategies include a vision for the development of a hydrogen industry (or its use as an energy source) out to 2030. However, the approach to setting shorter-term targets varies:

- the NSW Strategy only sets targets for 2030;

- the Victorian Plan sets objectives for a renewable hydrogen economy out to 2026, and will be reviewed every five years;

- the WA Strategy sets long term goals to 2030 and short-term goals to 2022;

- the Queensland Strategy and the National Strategy both set long term goals to 2030 and short term actions to 2025;

- the South Australian Plan does not include a timeframe;

- the NT Plan includes foundation plans to 2025 with further targets for 2035 and 2050;

- the TAS Action Plan establishes goals for the development of the hydrogen industry until 2030; and

- the ACT Paper (which is not a specific hydrogen strategy but discusses the use of hydrogen as part of the Territory's general renewable energy strategy) addresses sustainable energy policy from 2020 to 2025.

The varying time horizons for these strategies makes it difficult for investors and industry participants to track the progress of each state and territory in establishing a hydrogen industry. Jurisdictions with firm, quantitative targets over the short-to-medium term may prove favourable, as their targets are more likely to drive tangible action and provide interim opportunities for the relevant government to demonstrate its commitment to hydrogen. However, the nature of the targets (as set out in the following section) and the steps taken by the government to meet the targets will also play a significant role in building investor confidence.

Specific targets

We are only recently seeing the inclusion of specific targets in state and territory hydrogen plans and strategies. Due to the nascent status of the industry, many of the stated objectives have so far been at a very high level.

The more recent plans (like the NSW Strategy (October 2021), NT Plan (October 2021) and WA Strategy (updated in January 2021)) all include specific targets, whereas other states and territories take a more conceptual approach.

No specific targets, however sets key priorities.

To 2025: Foundations and Demonstrations

- Advance priority pilots, trials and demonstration projects.

- Assess supply chain infrastructure needs.

- Build demonstration-scale hydrogen hubs.

- Develop supply chains for prospective hydrogen hubs.

- Scale up support.

- Enabling activities.

From 2025: Large-Scale Market Activation

- Identify signals that large-scale hydrogen markets are emerging.

- Scale up projects to support export and domestic needs.

- Build Australian hydrogen supply chains and large-scale export industry infrastructure.

- Build and maintain robust and sustainable export and domestic supply chains (supply chain infrastructure includes powerlines, pipelines, storage tanks, refuelling stations, ports, roads, railway lines).

- Enable competitive domestic markets with explicit public benefits.

Measures of success by 2030 (among others):

- Australia is one of the top three exporters of hydrogen to Asian markets.

- Australia has an excellent hydrogen-related safety track record.

- Hydrogen is providing economic benefits and jobs in Australia.

- Australia has a robust, internationally accepted, provenance certification scheme in place.

- Hydrogen production and use is integrated into energy market structures.

Separately, the First Low Emissions Technology Statement 2020 set the target of generating clean hydrogen at under $2 per kg.

2030 Targets

- 110,000 tonnes of green hydrogen produced per annum.

- 12GW of renewable energy capacity.

- 700 MW of electrolyser capacity.

- Hydrogen priced at under AU$2.80/kg.

- 10,000 hydrogen vehicles in the NSW Government fleet.

- 100 refuelling stations.

- Gas network blending of 10%.

- 20% of the NSW Government's heavy vehicle fleet as hydrogen vehicles.

No specific targets, however sets key focus areas.

Foundation for renewable hydrogen

- Focuses on research and development, safety standards and regulation, innovation, workforce skills and sustainable water use.

Connecting the economy

- Gas networks have a pathway to renewable hydrogen.

- Renewable hydrogen enables the export of renewable energy.

- Integration of renewable hydrogen with the transport sector.

- Renewable hydrogen supports electricity system.

Leading the way

- Government support for renewable hydrogen pilots and projects.

- Government plays a significant role in coordinating across government and industry.

- Government uses its purchasing power to strengthen the renewable hydrogen sector.

- Victoria is a renewable hydrogen leader and promoted as a globally attractive trade and investment destination.

2022 Targets

- A project approved.

- Use of renewable hydrogen in one WA remote location.

- Distribution of renewable hydrogen in the gas network.

- Refuelling facility for hydrogen vehicles in WA.

2030 Targets

- WA export market share is similar to current LNG market share.

- WA gas network contains up to 10% renewable blend.

- Use of renewable hydrogen in mining haulage vehicles.

- Renewable hydrogen as a significant fuel source for transportation in regional WA.

No specific targets, however sets a vision that by 2030, Queensland will be at the forefront of renewable hydrogen production in Australia, supplying an established domestic market and export partners with a safe, sustainable and reliable supply of hydrogen.

Key focus areas are:

- Supporting innovation.

- Facilitating private sector investment.

- Ensuring an effective policy framework.

- Building community awareness and confidence.

- Facilitating skills development for a new technology.

No specific targets.

Rather, monitoring the following set of KPIs:

- Annual volume of hydrogen produced in SA.

- Annual volume of hydrogen exported overseas from SA.

- Cumulative capital investment in hydrogen infrastructure.

- Construction and ongoing jobs created.

Sets specific targets, including:

- Overall target of zero emissions by 2050.

- Microgrid hydrogen and solar pilots for remote communities within 2 years (ie by 2023)

- Competitively priced renewable energy delivered across networks within 5 years.

- Export scale renewable hydrogen by 2035 accounting for 15% of Australia's renewable export market.

- 70% or more renewable energy penetration in the Territory.

No specific targets.

Establishes goals for the development of the hydrogen industry until 2030.

From 2020-2024

- Commence production of renewable hydrogen, use locally produced renewable hydrogen in Tasmania and be well-advanced in developing export- based renewable hydrogen production projects.

From 2025-2027

- Commence export of renewable hydrogen.

From 2030 onwards

- Use locally produced renewable hydrogen as a significant form of energy in Tasmania and be a global producer and exporter of renewable hydrogen.

No specific targets.

The ACT Paper is a discussion paper on the ACT's sustainable energy policy generally, not a hydrogen policy specifically.

Green or blue?

Currently, one of the most hotly contested issues in the hydrogen space is whether governments should pursue 'green' hydrogen only (hydrogen made with renewable power, without fossil fuels) or also 'blue' hydrogen (hydrogen made with fossil fuels, but with emissions captured and stored, or offset). Some governments, like NSW, have expressed a commitment to green hydrogen only, citing consumer interests in totally clean energy and comparable price points. Other governments target 'renewable' hydrogen, with some explicitly including blue hydrogen in that category and others staying silent on whether renewable hydrogen covers blue hydrogen:

- the National Strategy focuses on 'clean' hydrogen, but explicitly includes blue hydrogen in its definition of renewable hydrogen and discusses carbon capture and storage as part of its plan;

- the NSW Strategy expresses a firm preference for green hydrogen in the short to medium term;

- the Victorian Plan focuses on the opportunities and benefits of renewable hydrogen, but does not indicate a preference of the Victorian Government between green hydrogen and blue hydrogen;

- the WA Strategy only refers to 'renewable hydrogen', however in other forums the government has recognised blue hydrogen as having 'a role in the transition';1

- the QLD Strategy focuses on exporting green hydrogen;

- the South Australian Plan does not express an explicit preference for green or blue hydrogen, however implies a preference for green hydrogen on the basis that it is more attractive to consumers seeking to reduce emissions;

- the NT Plan focuses on green hydrogen;

- the TAS Action Plan focuses on green hydrogen; and

- the ACT Paper highlights the need for renewable electricity for hydrogen production, evidently contemplating a green hydrogen industry.

The different preferences expressed by federal, state and territory governments may guide investors and developers as to the types of projects likely to receive greater support in each jurisdiction. However, a preference for one type of hydrogen production over another does not necessarily preclude projects utilising an alternative fuel source from proceeding.

Hydrogen price

Since the National Strategy was released, the Australian Government has made producing clean hydrogen for under $2 per kilogram ('H₂ under 2') a priority stretch goal under its first Low Emissions Technology Statement, as part of the broader Technology Investment Roadmap.2 A price point of less than $2 per kilogram is understood to be the point where hydrogen becomes competitive with alternative energy sources in large-scale deployment across our energy system.

While a number of state and territory strategies refer to the 'H2 under 2' target, only the NSW Strategy sets a specific price target. The NSW target is AU$2.80 per kilogram by 2030, with 'further cost reductions [to be] achieved through technology innovations and the falling cost of renewable energy to put us within reach of $2 per kilogram by the end of the decade'.3

Domestic consumption or export?

All state and territory hydrogen strategies (except for the ACT), and the National Strategy, contemplate hydrogen production for both domestic use and export to Asian markets – namely Japan, South Korea and China.

The National Strategy addresses both domestic consumption and export, however its 2030 measures of success have a strong focus on export. These include goals for Australia to be among the top three exporters of hydrogen to Asian markets, major offtake or supply chain agreements to be in place with importing countries, and to implement a robust, internationally-accepted certification scheme. The National Strategy also aims to have hydrogen production and use integrated into energy market structures in Australia.

The specific targets set out in the NSW Strategy focus on domestic consumption, particularly transport uses (eg the number of hydrogen-fuelled vehicles in the NSW government fleet and hydrogen refuelling stations by 2030) and gas network blending (eg 10% blending into gas networks by 2030). However, it also recognises the opportunity to export hydrogen produced in NSW, particularly to Japan and South Korea. One of the key principles is that an active domestic market for hydrogen will enhance NSW's export capacity.

The Victorian Strategy promotes hydrogen for both domestic use and export. In particular, it identifies the opportunity for hydrogen production using Victoria's offshore wind resources and subsequent export. The world's first hydrogen cargo was shipped from Port Hastings in Victoria in January 2022.

The WA Strategy promotes hydrogen for both domestic use and export. 2022 targets focus on domestic uses (including blending of hydrogen in the gas network and developing a hydrogen vehicle refuelling facility). The longer-term 2030 targets maintain this focus but also aim for WA's hydrogen export market share to be similar to its current LNG’s export market position.

The QLD Strategy recognises opportunities for hydrogen use both domestically and for export, however the focus tends towards export. The QLD Strategy aims to set Queensland up as the 'hydrogen exporter of choice for the world'.

The South Australian Plan addresses both domestic use and export, with a particular focus on export to South Korea, China and Japan.

The NT Plan addresses both domestic use and export. It targets the implementation of microgrid hydrogen and solar pilot projects for remote communities within two years after the strategy's publication (ie by 2023), while also aiming for renewable hydrogen exports from the Territory to account for 15% of Australia's renewable export market by 2050.

The TAS Action Plan addresses both domestic use and export, with its shorter-term goals to 2024 focusing on local use, and longer-term targets aiming for the export of renewable hydrogen from 2025 – 2027. From 2030 onwards, the TAS Action Plan wants locally produced hydrogen to be a significant form of state energy and for Tasmania to be a global producer and exporter of renewable hydrogen.

The ACT Paper focuses on the consumption of hydrogen in the ACT as part of its renewables strategy, rather than the production of hydrogen for export purposes.

Regulatory framework

Whilst all strategies acknowledge the need for an appropriate regulatory framework, only SA, NSW and WA have implemented specific legislative reforms to facilitate the development of a hydrogen industry.

SA

In February 2021, the Governor of South Australia declared hydrogen to be a regulated substance under the South Australian Petroleum and Geothermal Energy Act 2000, bringing hydrogen under the regulatory framework of the Act (including licensing, prohibited activities, royalties and so on). In June 2021, the South Australian Government tabled further amendments to the Petroleum and Geothermal Energy Act 2000, including:

- legislating for hydrogen and hydrogen by-products to be included in the definition of 'regulated substance' (rather than being declared a regulated substance through the Regulations);

- modifying the definition of transmission pipeline to allow for imported substances (such as manufactured hydrogen); and

- introducing Hydrogen Generation Licences to cover previously unregulated forms of generation (like electrolysis). This means hydrogen producers have access to the same regulatory and approvals scheme as existing petroleum and geothermal operators.

The Petroleum and Geothermal Energy (Energy Resources) Amendment Bill 2021 (SA) was tabled before the House of Assembly on 25 August 2021. It has not yet been passed.

NSW

On 19 November 2021, the Energy Legislation Amendment Bill was passed by Parliament. The Bill amends the Electricity Supply Act 1995, Energy and Utilities Administration Act 1987, Forestry Act 2012, Gas Supply Act 1996 and Pipelines Act 1967 to facilitate the development of a hydrogen industry.4 It includes amendments to:

- permit the Minister to grant exemptions from the Energy Savings Scheme under the Electricity Supply Act 1995 for electricity used to produce green hydrogen. This means that the electricity used to produce hydrogen will not be counted as a 'liable acquisition' and will not be factored into scheme participants' individual energy-saving targets (reducing their targets overall). This change is in addition to exemptions already available under the Peak Demand Reduction Scheme;

- exempt electricity loads using electricity to produce green hydrogen from contributing to the Climate Change Fund; and

- provide that regulations may be made to prevent a network service provider from recovering charges under a distribution determination or a transmission determination from a person who buys electricity to produce green hydrogen.

The NSW Strategy contemplates additional reforms yet to be introduced, including:

- green hydrogen will be exempt from contribution orders issued under the Electricity Infrastructure Investment Act 2020;

- transport laws, like the Dangerous Goods (Rail and Road) Transport Act 2008, Heavy Vehicle (Adoption of National Law) Act 2013 and the Transport Administration Act 1988, will be updated in preparation for the transport and distribution of hydrogen;

- gas laws, like the Gas Supply Act 1996, National Gas (New South Wales) Law 2008, Pipelines Act 1967 and Gas and Electricity (Consumer Safety) Act 2017, will be reviewed to ensure hydrogen can be used safely in the gas network; and

- the incorporation of special provisions relating to hydrogen production, distribution and use within Special Activation Precinct planning frameworks, with a view to enabling project approvals to be issued within 30 days.

WA

On 18 November 2021, the WA Government announced a new proposed form of land tenure – the ‘Diversification Lease’ – under the Land Administration Act 1997 (WA). The purpose of this new form of non-exclusive land tenure is to facilitate the development of hydrogen and renewable projects on pastoral lease areas and vacant Crown land.5 However, there is insufficient detail to determine the government's position on the development of these projects on mining tenements, where these projects would be unrelated to mining. Further information is available here.

Interaction with REZs

NSW, VIC, QLD, SA and TAS all have plans to develop REZs to facilitate the connection of renewable energy sources to electricity networks by co-locating essential infrastructure, logistics and resources. Of these, strategies in NSW, VIC, QLD and TAS specifically link REZ development with hydrogen production.

The Northern Territory is already working to transform its pre-existing Middle Arm Sustainable Development Precinct into a large-scale hydrogen export location (with expressions of interest to be sought from developers in 2022). Further, Western Australia plans to develop the Oakajee Strategic Industrial Area and has sought expressions of interest to develop renewable hydrogen projects within that area.6

Financial incentives

The public financial incentives available to proponents of hydrogen projects will influence the attractiveness of one jurisdiction over another for investment. Most of the various strategies and plans released by the states and territories provide high-level commitments to the types of financial support available to hydrogen industry participants. The incentives come in various forms, including grant rounds, loans, direct funding, matched funding commitments, in-kind support, and relief from various network and regulatory charges:

- The National Strategy commits $464 million to the Clean Hydrogen Industrial Hubs grant program, in addition to the ARENA Renewable Hydrogen Development Funding program, the CEFC Advancing Hydrogen Fund and the NERA Regional Hydrogen Technology Cluster Seed Funding Program.

- The NSW Strategy commits $750 million across three focus areas under the Net Zero Industry and Innovation Program and $70 million under the Hydrogen Hub Investment Scheme. Unspecified amounts of funding may also be made available through the Snowy Hydro Legacy Fund (total of $4.2 billion), the Regional Growth NSW Development Fund and project-specific funding arrangements. Separately, the NSW Strategy commits to twelve years of 90% concessions from network use of system charges and other energy security/decarbonisation scheme costs for hydrogen electrolysers from 2030.

- The Victorian Strategy's main financial incentive scheme is the Accelerating Victoria's Hydrogen Industry Fund ($10 million), which has run two grant programs so far – the Renewable Hydrogen Commercialisation Pathways Fund ($6.2 million for capital works investment) and the Renewable Hydrogen Business Ready Fund ($1 million for business strategy preparation).

- The WA Government has awarded grants from its $15 million Renewable Hydrogen Fund and proposed a matched funding commitment of $117.5 million with the Commonwealth (as part of the Commonwealth's Clean Hydrogen Industrial Hubs program) for two hydrogen hubs in the Pilbara and Mid West.

- The QLD Strategy and subsequent policy releases refer to the Queensland Hydrogen Industry Development Fund (which has awarded $12.57 million in funding and will award $10 million more), the Advance Queensland Initiative ($650 million) and the Queensland Renewable Energy and Hydrogen Jobs Fund ($2 billion). The Queensland government also released a useful Hydrogen Investor Toolkit.

- The South Australian Plan and subsequent policy releases flag three government funds investing in hydrogen development, including the Port Bonython Jetty Upgrade package ($37 million), the Grid Storage Fund ($50 million) and the Renewable Technology Fund ($150 million). In April 2021, South Australia also announced the State Energy and Emissions Reduction Deal with the Commonwealth, confirming an additional $442 million in funding from the South Australian Government.

- The Northern Territory's incentives have been limited to project-specific funding so far. We are not aware of any general funds having been announced.

- The TAS Action Plan promotes the Tasmanian Renewable Hydrogen Industry Development Fund, which has $20 million to award in grants, and a hydrogen fuel cell car trial with $2.3 million in funding. In addition, the Tasmanian Government is offering $20 million in concessional loans to support hydrogen projects and $10 million in support services, including payroll tax relief and more competitive electricity supply arrangements.

- The ACT has not announced any funding programs, however individuals can receive incentives for purchasing zero-emission passenger vehicles.

Actions you can take now

The release of hydrogen strategies and policies by every state and territory evidences the strong commitment of governments to seeing hydrogen play a major role in Australia's energy and export future. However, these strategies vary significantly, creating challenges for investors and industry participants attempting to stay on top of changes and make sense of the key differences. To be prepared for the hydrogen transition:

- consider where your business and objectives fit into the different strategic goals of each state or territory in terms of:

- any expressed preference for 'green' or 'blue' hydrogen;

- the location and development of REZs; and

- the different hydrogen applications prioritised by that state or territory (for example, export as pure hydrogen or ammonia, domestic use in fuel cells, passenger and heavy vehicle applications, or decarbonising emissions-intensive industries such as steel);

- continue to monitor announcements from the federal, state and territory governments regarding regulatory reforms and strategy updates to be prepared for changes to licensing regimes, certification schemes, safety standards, planning rules and the like. You can also monitor our Insight articles for regular updates on hydrogen developments (particularly in the regulatory space); and

- monitor grant funding rounds and further financial incentives announced by the various government departments overseeing public investment in hydrogen.

Footnotes

-

WA pledges $117m to stay in the global hydrogen race (watoday.com.au)

-

Angus Taylor MP, Fast Tracking renewable hydrogen projects (April 2020).

-

Department of Planning, Industry and Environment, NSW Hydrogen Strategy, p. 12.

-

Energy Legislation Amendment Bill 2021 (NSW), assented 29 November 2021.

-

Government of Western Australia, State government to unlock land for renewable energy and economic diversification (19 November 2021).

-

Oakajee Renewable Hydrogen Expression of Interest (www.wa.gov.au).